How Much Can I Borrow With a VA Loan?

Contents

Find out how much you can borrow with a VA Loan by using our VA Loan Calculator.

Checkout this video:

How Much Can I Borrow?

If you’re a veteran, you may be wondering how much you can borrow with a VA loan. The answer depends on a few factors, including the lender you’re working with and the county where the home is located. Generally speaking, you can borrow up to four times your entitlement, which is the maximum guarantee provided by the Department of Veterans Affairs.

The maximum loan amount is determined by the lender

The maximum loan amount for a VA home loan is determined by the lender. There is no maximum amount set by the Department of Veterans Affairs (VA), but the lender will only approve a loan up to a certain amount. This maximum loan amount varies from lender to lender and also from one VA county limit to another.

The largest factor in determining the maximum loan amount is the borrower’s ability to make monthly payments. The second largest factor is the value of the property. The VA’s county Loan Limits website provides more information on how much you can borrow with a VA loan.

The maximum loan amount is also determined by the appraised value of the property

The maximum loan amount that a Veteran can borrow is also determined by the appraised value of the property. The greater of the two calculations will be used to determine the maximum loan amount. In order to provide Veterans with the most accurate and up-to-date information, we have created a tool that will estimate your maximum loan amount based on your specific circumstances.

How Much of a Down Payment Do I Need?

For those that are looking to get a VA loan, one of the first questions they ask is how much they can borrow. The answer to this question can be found by understanding the ins and outs of the VA loan program.

No down payment is required

VA loans are powerful tools for homeownership. As part of the GI Bill, the VA loan program provides no-money-down financing for eligible active duty military and veterans. If you have at least a 620 credit score and steady income, you could qualify.

The VA does not set a minimum credit score requirement, but most lenders do. If you want to increase your chances of getting approved for a VA loan, aim for a credit score of at least 620. You can check your credit score for free with many online providers.

In addition to having a strong credit score, you’ll need to show that you have a steady income and enough money left over each month to cover your other expenses after paying your mortgage. The best way to do this is to get pre-approved by a lender so that they can help you estimate how much you can afford to borrow.

A down payment may be required if the appraised value is less than the purchase price

If you’re buying a home with a VA loan, you may need to make a down payment. Here’s how that works.

The Veterans Affairs (VA) loan program doesn’t require a down payment, but borrowers who put down less than 20% may have to pay for mortgage insurance. If your home’s appraised value is less than the purchase price, you’ll need to make a down payment equal to the difference plus any VA funding fee.

The VA funding fee is a one-time fee charged by the Department of Veterans Affairs to help cover the cost of the VA loan program. The fee is added to your loan balance and can be financed over the life of your loan.

For most borrowers, the funding fee is 2.3% of the loan amount. But if you’re making a down payment of less than 5%, the fee is increased to 3.6%. And if you’re eligible for a disability exemption, you may not have to pay the fee at all.

If you’re buying a home with a VA loan and you need to make a down payment, it’s important to know how much money you’ll need to bring to the table.

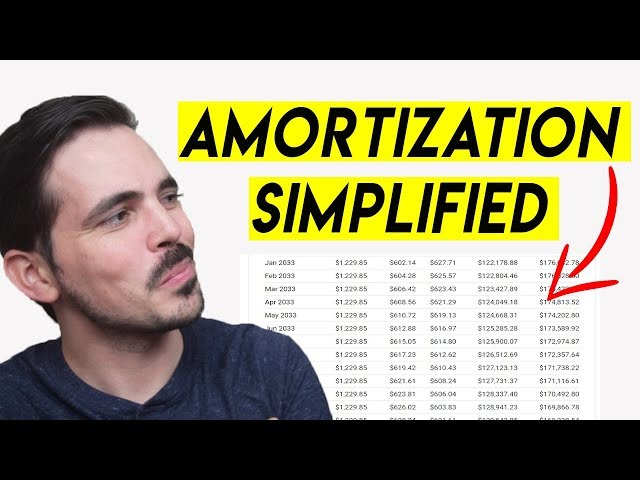

How Much Will My Monthly Payment Be?

Your monthly payment may vary depending on the specific terms of your loan, but you can get a general idea of how much it will be by using a VA loan calculator. Your monthly payment will be determined by your loan amount, interest rate, and loan term. The longer your loan term, the lower your monthly payments will be, but you will pay more in interest over the life of the loan. You can also choose to make a lump sum payment to reduce the interest paid on the loan.

The monthly payment is determined by the loan amount, the interest rate, and the loan term

The monthly payment is generally determined by three things – the loan amount, the interest rate, and the loan term.

The loan amount is the principal – how much you are borrowing. The interest rate is what you will pay each year on that principal, expressed as a percentage. The loan term is how long you have to pay back the loan – usually 15 or 30 years.

To calculate your monthly payment, you would take the loan amount, multiply it by the interest rate (expressed as a decimal), and then divide that number by 12 to get your monthly payment.

For example, if you were borrowing $100,000 at an interest rate of 5%, your monthly payment would be $416.67 (($100,000 x 0.05) / 12).

You can use an online calculator to help you estimate your monthly payment.

How Much Can I Borrow With a VA Loan?

The maximum loan amount is determined by the lender

The Department of Veterans Affairs does not impose a maximum loan amount on VA loans. However, lenders who fund the loans will have their own maximums. For 2019, most lenders limit VA loans to a maximum of $484,350 for a no-money-down loan. That’s the “floor” or “baseline” limit for conforming conventional home loans.

The maximum loan amount is also determined by the appraised value of the property

The maximum loan amount for a VA loan is determined by the appraised value of the property. In general, the appraised value is equal to the purchase price of the home. However, there are certain circumstances in which the appraised value may be higher or lower than the purchase price.