How Credit Scoring Works: The Basics

Contents

Find out how credit scoring works and what factors are used to calculate your score.

Credit Scoring Works: The Basics’ style=”display:none”>Checkout this video:

What is a credit score?

A credit score is a numerical expression that is used to determine your creditworthiness. This number is important because it is used by lenders to decide whether or not to give you a loan. Credit scores are calculated by using information from your credit report . This information is then used to calculate your score.

The history of credit scoring

Most people have a general idea of what a credit score is: A number that represents your creditworthiness. But what does that number actually mean? And, more importantly, where did it come from?

A credit score is a numerical representation of your credit risk. The higher your score, the lower your risk. Credit scores are used by lenders to determine whether or not to lend you money, and also influence the interest rate you’ll pay on a loan.

The first credit scoring system was developed in the mid-1950s by Bill Fair and Earl Isaac, two pioneering thinkers in the field of risk management. Their company, Fair Isaac Corporation (now FICO), designed a scoring system that could be used to predict whether or not a person would repay their debt. This system was based on data from millions of consumers, and was constantly refined as new data became available.

Today, FICO scores are used by 90% of top lenders to make lending decisions. But FICO is just one of many credit scoring models out there. Other companies, such as VantageScore and Experian, have developed their own scoring systems, which are also used by lenders to determine creditworthiness.

While each scoring system is slightly different, they all serve the same basic purpose: To give lenders insight into your credit risk. So whether your score comes from FICO, VantageScore, or Experian, it’s still an important number to pay attention to.

How credit scores are calculated

Most credit scoring models use a similar formula to generate a credit score. The most popular credit scoring model is the FICO score, which is used by major credit bureaus including Equifax, Experian and TransUnion.

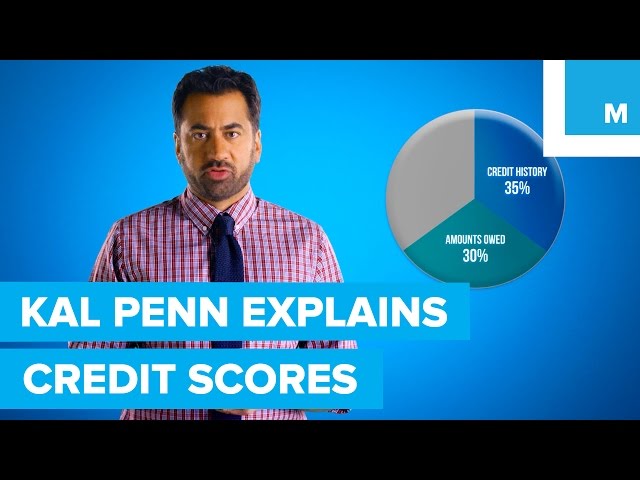

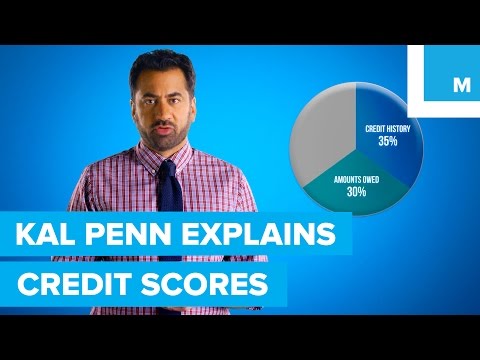

There are five main factors that are used to calculate a FICO score:

-Payment history (35%)- This is the most important factor in your score. Payment history includes paying bills on time, as well as any negative marks such as collections, bankruptcies or late payments.

-Utilization (30%)- This refers to the amount of credit you are using compared to your credit limit. A lower utilization ratio is better for your score.

-Credit history (15%)- The length of your credit history makes up 15% of your FICO score. A longer history indicates to lenders that you’re a less risky borrower.

-Credit mix (10%)- This measures the variety of different types of credit accounts you have, such as revolving lines of credit, installment loans or mortgages. Having a mix of different types of accounts can improve your score.

-New credit (10%)- This measures how often you have applied for new lines of credit recently. Applying for too much new credit at once can be a red flag for lenders and lower your score.

The importance of credit scores

Your credit score is a three-digit number that lenders use to decide whether to give you a loan and how much interest to charge. A high score means you’re a low-risk borrower, which could lead to a lower interest rate on a loan. A low score could lead to a higher rate.

How credit scores affect your life

Credit scores are important because they affect your ability to borrow money. A high credit score means you’re a low-risk borrower, which could lead to a lower interest rate on a loan. A low credit score could lead to a higher interest rate and could mean that you won’t be approved for a loan at all.

A good credit score is anything above 700, and a excellent credit score is 760 or higher. FICO, the company that creates the credit scores used by lenders, has a scale that goes from 300 to 850; the higher the number, the lower the risk you are to lenders.

For example, let’s say you’re applying for a loan with an interest rate of 10%. If you have a good credit score, you may be able to qualify for an 8% interest rate. That may not seem like much of a difference, but over the life of a five-year loan, you would save $2,587 in interest payments by getting the lower rate.

Your credit score also affects how much you’ll pay for car insurance. Studies have shown that people with poor credit are more likely to file insurance claims than people with good credit. As a result, insurers charge people with poor credit more for their coverage. In some states, insurers can charge people with poor credit up to twice as much as people with good credit.

The benefits of having a good credit score

Credit scores are important because they give lenders a quick, objective way to assess your creditworthiness. A high credit score signals to lenders that you’re a good bet to repay your debts on time and in full. This could mean you’re eligible for lower interest rates and better terms on loans and credit cards. Conversely, a low credit score could lead to higher interest rates and less favorable terms.

A strong credit score also puts you in a better position to negotiate favorable loan terms. Lenders typically offer their best rates and terms to borrowers with strong credit scores. So, if you have good credit, you may be able to get a lower interest rate even if you don’t shop around for the best deal.

Generally speaking, the higher your credit score, the more access you’ll have to credit at the most favorable terms. A higher score can also give you more negotiating power with landlords, utilities companies, and cell phone providers — basically anyone who does a routine check of your credit as part of their decision-making process.

The different types of credit scores

There are a few different types of credit scores out there. The most common are FICO® Scores and VantageScores. FICO® Scores are the credit scores most lenders use to make credit decisions. VantageScores are credit scores developed by the three major nationwide credit reporting agencies: Equifax, Experian and TransUnion.

FICO scores

FICO scores are the most widely used credit scores, and they’re calculated by Fair Isaac Corporation. There are actually dozens of different FICO scores, but the most common ones used by lenders are the FICO® 8 scoring model and its successors.

FICO® 8 is the scoring model most often used in lending decisions, and it’s the one you’re most likely to see when you check your own credit score. However, some lenders may still be using older versions of the FICO® score, such as FICO® 5 or FICO® 2.

The newest version of the FICO® score is called the UltraFICO™ score, and it’s designed to help people with limited credit histories get approved for loans and credit cards.

VantageScore

VantageScore is a scoring system developed jointly by the three major credit bureaus – Experian, TransUnion and Equifax. It’s designed to provide a more consistent and transparent credit scoring system, particularly for consumers who don’t have a lot of traditional credit history.

VantageScore was first introduced in 2006, with the most recent version – VantageScore 3.0 – rolling out in 2013. One of the key features of VantageScore is that it’s built on the same credit reporting data used by FICO, so it should be just as accurate. In fact, according to MyFICO, VantageScore 3.0 scores should only differ from FICO scores by about 10 points on a 300 to 850 scale.

Like FICO scores, VantageScores range from 300 to 850 and are based on six key factors:

-Payment history (35%)

-Credit utilization (30%)

-Credit age (15%)

-Total accounts (10%)

-Mix of credit types (10%)

Other types of credit scores

There are several other types of credit scores that are used for different purposes. Here are some of the most common:

Auto insurance scores: Auto insurance companies use credit information to help determine rates. Studies have shown that people with higher scores are less likely to file claims.

Employment screening scores: Some employers use credit information as part of their screening process for new employees. They believe that people who manage their credit well are more likely to be responsible and dependable employees.

Landlord scores: Landlords sometimes use credit information to screen applicants for rental housing. They believe that people with good credit are more likely to pay their rent on time and take care of the property.

utility scores: Utilities sometimes use credit information to screen applicants for service. They believe that people with good credit are more likely to pay their bills on time and be less likely to default on their payments.

How to improve your credit score

Your credit score is a number that represents your creditworthiness. It is used by lenders to determine whether you are a good candidate for a loan and what interest rate you will be charged. A higher credit score means you are a lower-risk borrower, which could lead to a lower interest rate on a loan. There are a few things you can do to improve your credit score.

Steps to take to improve your credit score

There are a number of things you can do to improve your credit score. Here are some steps you can take:

1. Review your credit report for accuracy. You can get a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months at AnnualCreditReport.com. Dispute any errors you find with the credit bureau in question.

2. Make all of your payments on time. This is the most important factor in determining your credit score. Payment history makes up 35% of your FICO® Score—the credit score most lenders use—so it’s important to keep tabs on this information. You can set up payment reminders through your financial institution or sign up for auto-pay to ensure that your bills are always paid on time.

3. Keep balances low on credit cards and other revolving credit accounts. Your credit utilization ratio—the percentage of available credit you’re using—accounts for 30% of your FICO® Score calculation, so it’s important to keep this number low. Expert advice generally recommends using no more than 30% of your available credit, but the lower the better. If you have a balance that you can’t pay off in full each month, consider making more than the minimum payment until the balance is repaid in full.

4. Apply for and open new credit accounts only as needed. Having too many new accounts can lengthen the time it takes to rebuild your credit history and improve your score, so only apply for new lines of credit when absolutely necessary—and make sure you’re able to manage any new debt responsibly.

5. Use a mix of different types of loans and lines of credit including auto loans, mortgages, student loans, and personal loans/lines of credit. A diverse mix helps show that you’re a responsible borrower and helps improve your chances of qualifying for future lines of credit at more favorable terms—even if you don’t need them right now

The importance of monitoring your credit score

Your credit score is a number that reflects the risk you pose to lenders. The higher your score, the less risk you pose, and the more likely you are to be approved for a loan or credit card. Conversely, the lower your score, the more risk you pose, and the less likely you are to be approved.

That’s why it’s so important to monitor your credit score regularly. You can get your free credit report from AnnualCreditReport.com, and you can check your credit score for free on sites like CreditKarma.com or CreditSesame.com. By regularly monitoring your score, you’ll be able to catch any mistakes that might lower your score, and you’ll also be able to spot any potential fraud early on.