How Your Credit Score Works

Contents

Find out how your credit score is calculated and what steps you can take to improve your credit rating.

Credit Score Works’ style=”display:none”>Checkout this video:

How Credit Scores Are Calculated

Credit scores are designed to give lenders a snapshot of your creditworthiness, or how likely you are to repay a loan. A credit score is calculated based on your credit history, which is a record of your borrowing and repayment activity. The information in your credit history is used to generate a credit score that lenders can use to assess your creditworthiness.

Payment history

One of the most important factors in your credit score is your payment history. This includes whether you’ve paid your bills on time, as well as any history you have of making late payments, declared bankruptcy, or having accounts sent to collections.

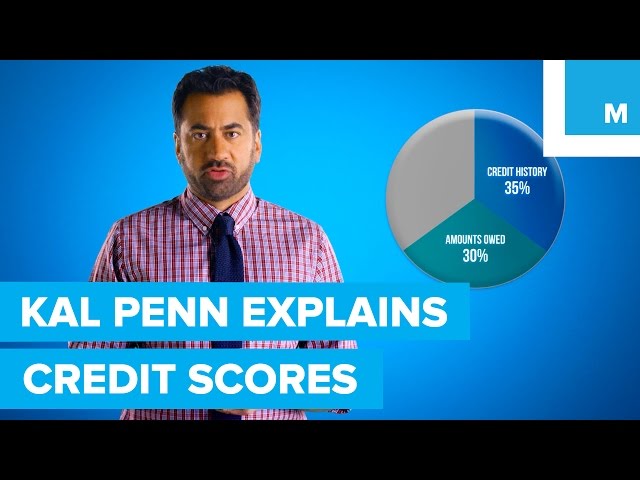

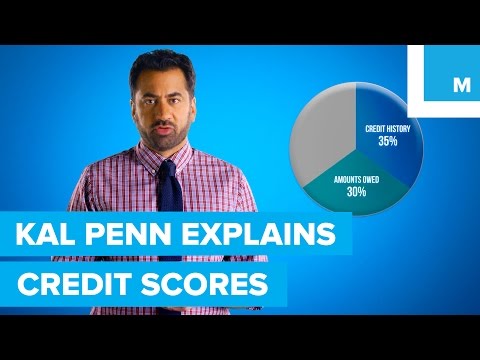

Your payment history makes up 35% of your FICO® Score—that’s more than any other factor. So, if you have a long history of making payments on time, you’ll probably have a good FICO® Score. Late or missed payments will lower your score, and can stay on your credit report for up to seven years.

Types of debt

There are two types of debt that can appear on your credit report: installment debt and revolving debt. Installment debt includes auto loans, student loans and mortgages. These debts have a set end date for repayment, and the monthly payments are usually the same each month. Revolving debt includes credit cards and lines of credit. With this type of debt, you have a set credit limit, but your monthly payment can vary based on how much you owe that month.

Length of credit history

One of the key factors that makes up your credit score is the length of your credit history. This is a metric that looks at how long you have had active lines of credit — such as credit cards, loans, and so on.

The idea behind this metric is that people with longer credit histories are generally more responsible borrowers than those who have shorter histories. This is because they have had more time to establish a track record of making on-time payments, maintaining low balances, and so on.

As a result, lenght-of-credit-history makes up approximately 15% of your FICO score — which is the most commonly used type of credit score. So, it’s clearly an important factor in determining your score.

There are a few things you can do to help improve your length-of-credit-history metric:

1) If you have any inactive lines of credit, consider reactivating them.

2) If you have any new lines of credit, use them responsibly to help establish a good payment history.

3) Keep your oldest lines of credit open — even if you don’t use them often. This will help lengthen your credit history.

New credit

New credit makes up 10% of your score. Opening several credit accounts in a short period of time can hurt your score.

Your score is also hurt if you’re “maxing out” your credit cards. You’re using too much of your available credit when you do this, and it sends a red flag to creditors that you might be in financial trouble.

Keeping your credit balances low relative to their limits will help your score. So will having a mix of both types of credit accounts, such as a mortgage, an auto loan and a few credit cards.

Credit mix

Credit mix accounts for 10% of your FICO® Score and is based on the types of credit accounts in your credit report. A varied credit mix (for example, a mix of installment loans, such as a mortgage or auto loan, and revolving lines of credit, such as a credit card) can help you build good credit.

How to Improve Your Credit Score

Your credit score is a key factor in determining whether you will be approved for a loan, and if so, what interest rate you will be offered. A high credit score indicates to lenders that you are a low-risk borrower, which means you are more likely to be approved for a loan and to receive a lower interest rate. There are a number of things you can do to improve your credit score.

Check your credit report for errors

One of the best ways to improve your credit score is to check your credit report for errors and dispute any that you find. You’re entitled to one free credit report from each of the major credit bureaus — Experian, Equifax and TransUnion — every 12 months. You can get yours by visiting annualcreditreport.com or by calling 1-877-322-8228.

When you review your report, look for errors in your personal information, such as your name, address, Social Security number or date of birth. Errors could also be in your credit history, like accounts that don’t belong to you or late payments that have been incorrectly reported. If you find an error on your credit report, you can file a dispute with the credit bureau.

You should also check your credit report for negative items that could be dragging down your score, such as late payments, collections accounts or bankruptcies. If you see anything that isn’t accurate or needs to be updated, you can dispute it with the credit bureau.

Pay your bills on time

One of the most important things you can do to improve your credit score is to always pay your bills on time. Your payment history is the biggest factor in your credit score, so even if you have a low credit score, you can improve your credit score just by paying your bills on time from now on. If you have missed payments in the past, try to make up for it by making extra payments or using a service like autopay to make sure you never miss a payment again.

Your credit score is important because it’s used by lenders to decide whether or not to lend you money. A good credit score means you’re more likely to be approved for loans and credit cards, and you’ll probably get better terms (like lower interest rates) if you are approved. A bad credit score might mean you’re denied for loans and credit cards, or you might only be approved for loans with very high interest rates.

Reduce your credit card balances

Your credit utilization – or how much of your available credit you’re using – makes up 30% of your credit score. That’s why it’s so important to keep your balances well below 30% of your credit limit (10% is even better).

If you have multiple credit cards, work on paying down the balances on the card with the highest interest rate first. Or, if you have one card with a very low balance and another with a high balance, work on paying down the high balance first. By tackling the card with the highest interest rate or highest balance first, you’ll save the most money in interest charges.

Diversify your credit mix

One way to help improve your credit score is by diversifying your credit mix. This means having a variety of different types of credit accounts, such as a mix of both revolving (credit cards) and non-revolving (personal loans) accounts. This shows lenders that you can manage different types of credit responsibly.

Limit your credit inquiries

One of the most common questions we hear is “how can I improve my credit score?” There are a number of things you can do to improve your credit score, but one of the most important is to limit your credit inquiries.

When you apply for a new credit card or loan, the lender will look at your credit report and take what’s called a “hard pull.” This means that they are pulling your credit report with the intention of making a decision about whether or not to approve you for the loan or credit card.

Each time a lender does a hard pull on your credit report, it can ding your score by a few points. So if you’re looking to improve your score, it’s important to limit the number of hard pulls you have on your report.

Of course, there are some instances where you may need to have a hard pull on your report. For example, if you’re applying for a mortgage or car loan, the lender will likely do a hard pull as part of their decision-making process. In these cases, it’s important to shop around and compare rates from multiple lenders before settling on one; this way, you can minimize the impact on your score.

In short, if you’re looking to improve your credit score, one of the best things you can do is limit the number of hard inquiries on your report.