How Does Your Credit Score Work?

Contents

A credit score is a number that credit agencies use to determine your creditworthiness. Find out how your credit score is calculated and what you can do to improve it.

Checkout this video:

What is a credit score?

A credit score is a number that represents your creditworthiness. It’s used by lenders to determine whether you’re a good candidate for a loan. The higher your score, the more likely you are to be approved for a loan.

How is your credit score calculated?

There are many different credit scoring models, but the most common one used by lenders is the FICO score . It was created by the Fair Isaac Corporation, and it ranges from 300 to 850. The higher your score, the lower your interest rate is likely to be.

Your FICO score is calculated using five different factors:

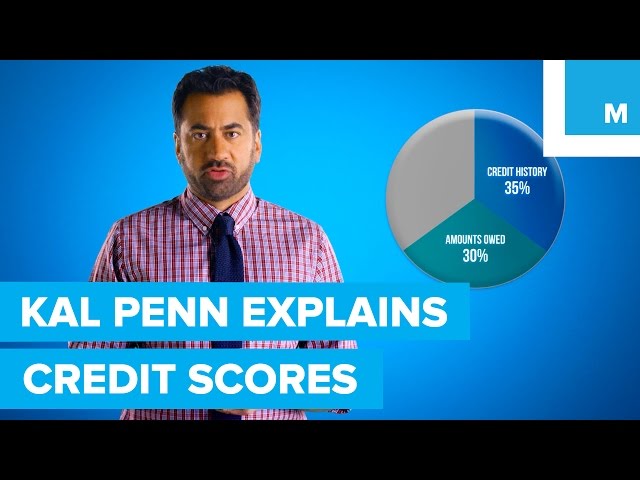

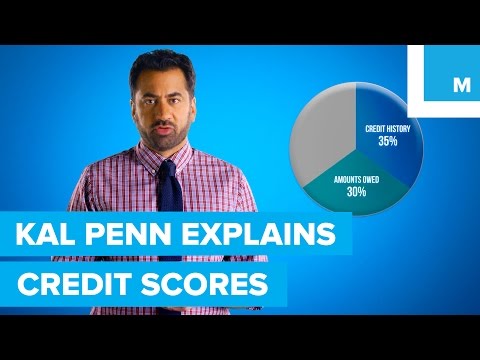

-Payment history (35%)- Do you have a history of making late payments or missing payments altogether?

-Credit utilization (30%)- This is how much of your available credit you are using at any given time. It’s important to keep this number low, around 30% or less.

-Credit history length (15%)- A longer credit history will generally result in a higher credit score.

-Credit mix (10%)- This refers to the types of credit accounts you have, such as credit cards, mortgages, etc.

-New credit (10%)- Having too many new lines of credit can be viewed as a red flag by lenders.

What factors influence your credit score?

There are many factors that can influence your credit score. Some of the most common include your payment history, credit utilization, credit mix, and length of credit history. Let’s take a closer look at each of these.

Payment history

Your payment history is one of the most important factors in your credit score—making up 35% of your FICO® Score☉ —so it’s important to know how it works.

Your payment history includes information about whether you’ve made all your payments on time, and if you haven’t, how late your payments were and how many times you’ve missed payments. This information comes from your credit report, which is a record of your credit activity that includes information about your loans and lines of credit, as well as whether you pay them on time.

Making late or missing payments can negatively impact your credit score, so it’s important to try to make all your payments on time. If you have trouble doing this, there are some things you can do to try to improve your payment history, including:

-Setting up automatic payments from your bank account so you don’t have to remember to make a payment each month

-Making a budget and sticking to it so you know how much money you have available to pay your bills each month

-Asking for a lower interest rate from your creditors so you have more money available each month to put towards your payments

-Calling your creditors if you think you might miss a payment and asking them if they can work with you

Credit utilization

Credit utilization is one of the most important factors in credit score calculation, and refers to the amount of debt you have in relation to your credit limit. In general, it’s best to keep your utilization below 30%, and ideally below 10%. The lower your debt in relation to your credit limit, the better it is for your score.

Length of credit history

One factor that influences your credit score is the length of your credit history. Your credit score takes into account all of the accounts you have open and the payments you have made on those accounts. The longer your history of responsible credit use, the better your score will be.

Types of credit

Payment history (35%): Do you make your payments on time? This is the single biggest factor in your score.

Amounts owed (30%): How much debt do you have compared with your credit limits? The lower your balances, the higher your score.

Length of credit history (15%): A long credit history generally helps your score.

Credit mix (10%): Having a mix of different types of debt, such as a mortgage, car loan and student loan, can help your score.

New credit (10%): Opening several new accounts in a short period can lower your score.

How can you improve your credit score?

Your credit score is important because it is one factor that lenders look at when considering you for a loan. A high credit score means you’re a low-risk borrower, which could lead to a lower interest rate on a loan. There are a few things you can do to improve your credit score.

Make your payments on time

One factor that weighs heavily into your credit score is your payment history. Payment history accounts for 35% of your FICO® Score.

Your payment history includes all the payments you’ve made on time as well as any late payments or collections items. Any time you make a late payment, fail to pay a collection item or have a public record such as a bankruptcy, foreclosure or tax lien, this information will show up on your credit report and could potentially drag down your credit score.

This is why it’s important to make all your payments on time, every time. Even if you can only afford the minimum payment, make sure you pay by the due date to avoid any negative marks on your credit report.

Keep your credit utilization low

One of the best ways to improve your credit score is to keep your credit utilization low. Credit utilization is the percentage of your available credit that you are using. For example, if you have a credit limit of $1,000 and you owe $500, your credit utilization is 50%.

Ideally, you should keep your credit utilization below 30%. The lower it is, the better it is for your credit score. If you can keep it below 10%, that’s even better.

There are a few ways to lower your credit utilization. One is to simply pay down your balances. Another is to ask for a higher credit limit from your creditor. If you have a good history with them, they may be willing to increase your limit.

You can also spread out your debt by opening new accounts. This will give you more available credit and lower your credit utilization. But be careful with this one. You don’t want to open too many new accounts at once, as this could be seen as a sign of financial distress and hurt your score in the long run.

Use a mix of different types of credit

Different types of credit include credit cards, store cards, auto loans, personal loans, and mortgages. Lenders like to see that you’re capable of managing different types of credit responsibly. This shows them that you’re likely to repay your loans on time.

If you only have one type of credit (like a credit card), you’re seen as a higher risk to lenders. This is because it’s easy to max out a credit card and make late payments, but it’s much harder to do this with a mortgage. So, using a mix of different types of credit can help improve your credit score.

How can you check your credit score?

There are a few ways you can check your credit score. You can go to AnnualCreditReport.com to get a free credit report from each of the three major credit bureaus . You can also use a credit monitoring service like Credit Karma or Experian. And finally, you can check your credit score directly with the credit bureau.

Use a credit monitoring service

If you’re looking to keep tabs on your credit score, you can do so by using a credit monitoring service. Credit monitoring services will help you stay up to date on your credit score and report any changes that have occurred. Additionally, many credit monitoring services offer tools and resources that can help you improve your credit score.

Check your credit report

The best way to check your credit score is to request a free credit report from one or more of the three major credit reporting bureaus: Experian, Equifax and TransUnion. You’re entitled to a free report from each bureau once every 12 months. You can request your report online, by phone or by mail.

If you find errors on your credit report, you can dispute them with the credit bureau. This process can take awhile, but it’s important to get inaccuracies removed from your record so they don’t drag down your score.

You can also get a free credit score from several personal finance websites, including Credit Karma, Credit Sesame and Quizzle. These scores are based on the information in your credit reports, but they may not be identical to the scores lenders use when considering your loan application.