What Is a Finance Charge on a Loan?

Contents

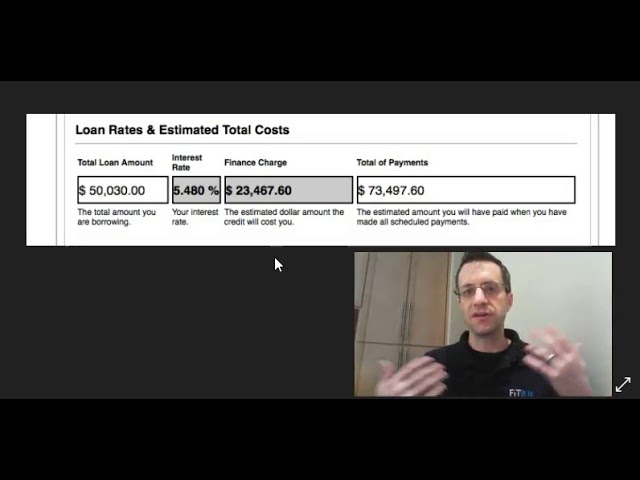

A finance charge is the cost of borrowing money. The charge is expressed as an annual percentage rate (APR). The APR is the cost of borrowing money for one year, including interest, fees, and other costs.

Checkout this video:

What is a finance charge?

A finance charge is a fee charged by a lender for the use of credit. The finance charge is calculated as a percentage of the total loan amount and is typically paid at the time of loan disbursement.

Finance charges can be either fixed or variable, and may be paid in installments or as a lump sum. Common examples of finance charges include interest charges, processing fees, and origination fees.

Finance charges are generally expressed as an Annual Percentage Rate (APR), which includes the interest rate plus any additional fees charged by the lender. For example, a loan with an APR of 10% would have an interest rate of 9% and an additional 1% fee for the use of credit.

How is the finance charge calculated?

The finance charge on a loan is the total cost of borrowing money from a lender. It includes interest charges as well as any other fees or charges associated with the loan. The finance charge is expressed as a percentage of the total loan amount and is typically disclosed to borrowers in the loan agreement.

How is the finance charge calculated?

The finance charge on a loan is calculated using the interest rate and the amount of time borrowed. It is important to note that the finance charge does not include any fees charged by the lender, such as origination fees or closing costs. The annual percentage rate (APR) is a good way to compare different loans because it takes into account both the interest rate and the finance charges.

What are some common ways to avoid finance charges?

Here are some common ways to avoid finance charges on a loan:

-Make your payments on time: This is the most important way to avoid finance charges.

-Pay more than the minimum payment: Paying more than the minimum payment will help you pay off your loan balance faster and avoid interest charges.

-Refinance your loan: If you have a high interest rate, you may be able to refinance your loan to get a lower rate and save on finance charges.

– Shop around for the best rates: Compare rates from different lenders to make sure you’re getting the best deal.

What are some common finance charges?

Included in the finance charge may be the following:

-Interest. This is the fee you pay to borrow money. The annual percentage rate (APR) is the interest rate plus any other fees charged as a percentage of the loan amount.

-Service or maintenance fees. You may be charged a monthly or annual fee to maintain your account.

-Loan origination fee. This is a one-time fee charged when you first take out a loan. It covers the lender’s administrative costs in processing your loan application and generating the paperwork.

-Discount points. You may be able to buy down your interest rate by paying discount points when you first take out a loan. Each point typically costs 1 percent of your loan amount.

-Document preparation fee. You may be charged for the costs incurred by the lender in preparing your loan documents.

-Appraisal fee. If you’re taking out a home equity loan, you may have to pay for an appraisal of your property’s value.

What are some tips for managing finance charges?

Finance charges can be a significant cost on loans, so it’s important to understand how they work and how to manage them. Here are some tips:

-Read your loan agreement carefully. It should include information on the finance charge, how it’s calculated, and when it will be applied to your account.

-Know when your grace period ends. This is the time (usually 20-30 days) when you can avoid finance charges by paying your entire balance. Once the grace period ends, any unpaid balance will start accruing finance charges.

-Pay more than the minimum payment each month. This will help you pay off your balance faster and avoid paying interest charges over the life of the loan.

-Keep track of your balance and payments so you can calculate the finance charges yourself. This way you can budget for them and be prepared when they appear on your statement.

-If you’re having trouble making payments, contact your lender as soon as possible to discuss options for avoiding late fees or defaulting on the loan.