Who Qualifies for a Student Loan?

Contents

If you’re wondering whether you qualify for a student loan, the answer is probably yes. In fact, most people who attend college or university will qualify for some form of financial aid.

Checkout this video:

Student Loans

You may be able to get a student loan if you’re enrolled in an eligible course at an approved higher education provider, and you’re: an Australian citizen, or the holder of a permanent humanitarian visa, or a New Zealand citizen. Depending on the type of course you’re studying, you may get a Commonwealth supported place or a fee-paying place.

How to Apply

You can apply for a federal student loan by completing the Free Application for Federal Student Aid (FAFSA®) form. Your school will use your information from the FAFSA form to determine how much financial aid you’re eligible to receive.

To complete the FAFSA form, you (and your parents, if you’re a dependent student) will need to gather financial information, including:

-Your Social Security number

-Your parents’ Social Security numbers (if you’re a dependent student)

-Your driver’s license number (if any)

-Your Federal Student Aid PIN

-Federal tax information or tax returns, including W-2 forms—for you (and your parents, if you’re a dependent student)

-Bank statements and records of investments (if any)

-Records of untaxed income (if any)

Once you have this information, visit fafsa.ed.gov to fill out and submit your FAFSA form online. If you prefer, you can get a paper FAFSA form from your school or by contacting the Federal Student Aid Information Center.

Types of Loans

There are four types of Direct Loans available:

-Direct Subsidized Loans are awarded based on financial need. The U.S. Department of Education pays the interest that accrues on a Direct Subsidized Loan while you’re in school at least half-time, during your grace period, and during deferment periods.

-Direct Unsubsidized Loans are not based on financial need. The U.S. Department of Education does not pay the interest that accrues on a Direct Unsubsidized Loan while you’re in school at least half-time, during your grace period, or during deferment periods. You are responsible for paying the interest that accrues on a Direct Unsubsidized Loan from the time the loan is disbursed until it is paid in full.

-Direct PLUS Loans are awarded to graduate or professional students and parents of dependent undergraduate students to help pay education expenses not covered by other financial aid. The U.S. Department of Education pays the interest that accrues on a Direct PLUS Loan while you’re in school at least half-time, during your grace period, and during deferment periods for Direct PLUS Loans first disbursed on or after July 1, 2008, and before July 1, 2010) OR during forbearance periods (for Direct PLUS Loans first disbursed before July 1, 2008). You are responsible for paying the interest that accrues on a Direct PLUS Loan from the time the loan is disbursed until it is paid in full unless you choose to have this interest capitalized (added to your outstanding principal balance) when repayment begins six months after you graduate or leave school OR if you allow your loan to enter into forbearance (for Direct PLUS Loans first disbursed before July 1, 2008).

-Direct Consolidation Loan allows you to combine all of your eligible federal student loans into a single loan with a fixed interest rate for the life of the loan.

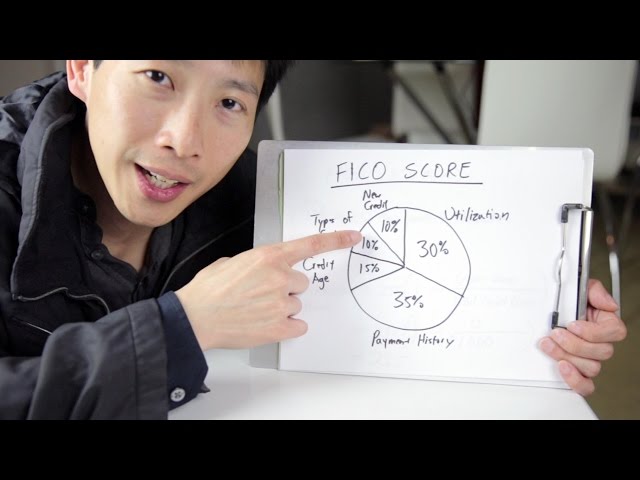

Who Qualifies

While many factors play a role in the qualification process for a student loan, the two most important factors are credit score and income. If you have a strong credit score, you are more likely to qualify for a loan with a lower interest rate. If you have a higher income, you are more likely to qualify for a larger loan.

Students Who Demonstrate Financial Need

A student who demonstrates financial need is eligible for a student loan. The amount of money a student receives from the loan will be based on their financial need and the cost of attendance at their school.

Students Who Don’t Demonstrate Financial Need

For federal student loans, you don’t have to demonstrate financial need to qualify. The federal government offers both need-based and non-need-based loans.

Most federal student loans are awarded based on financial need. To qualify, you must first fill out a Free Application for Federal Student Aid (FAFSA®) form.

Loans that don’t require an application for financial aid, such as the PLUS loan for graduate students and parents and the unsubsidized Direct Loan, are considered non-need-based loans. You can get these types of loans even if you have a low income or no income at all.

Private Student Loans

To qualify for a private student loan, you will typically need to have good or excellent credit. Some lenders may also require a co-signer who also meets these credit requirements. In addition, you will need to prove that you have the financial ability to repay the loan by providing documentation of your income and employment history.

Applying for Student Loans

Applying for a student loan can be a daunting task, but it doesn’t have to be. The first step is to research the different types of loans available and to find the one that best suits your needs. There are many different types of student loans, so it’s important to find the one that’s right for you. Next, you’ll need to fill out a Free Application for Federal Student Aid (FAFSA) form. This form will help you determine your eligibility for federal student aid.

Applying for Federal Student Loans

Federal student loans are funded by the U.S. Department of Education and they come with several benefits including fixed interest rates, income-driven repayment plans, and loan forgiveness programs. You can apply for federal student loans through the Free Application for Federal Student Aid (FAFSA).

To be eligible for federal student loans, you must:

– Be a U.S. citizen or eligible non-citizen

– Have a valid Social Security number

– Be enrolled in an eligible degree or certificate program at least half-time

– Not be in default on any previous federal student loans

– Not have exceeded your lifetime limit for federal student loan borrowing

Applying for Private Student Loans

If you’re considering a private student loan, your first step is to fill out a Free Application for Federal Student Aid, or the FAFSA. This form is used to determine your eligibility for federal student aid, which includes grants, work-study and federal loans.

The FAFSA will also be used by your school’s financial aid office to determine your eligibility for need-based aid, such as need-based grants and scholarships.

To complete the FAFSA, you (and your parents, if you’re a dependent student) will need to gather some financial information, including your bank statements, tax returns and W-2 forms. You can get help filling out the FAFSA from the Department of Education’s FAFSA website or from your school’s financial aid office.

Once you have completed the FAFSA, you will receive a Student Aid Report (SAR), which will provide information on your expected family contribution (EFC). Your EFC is the amount of money that you and your family are expected to contribute to the cost of your education.

The next step is to research private student loan options and compare interest rates and terms. Keep in mind that private student loans should be used as a last resort, after you have exhausted all other financial aid options.

When you have found a private student loan that meets your needs, you will need to complete a loan application and provide information on yourself, your co-signer (if applicable) and your school. The lender will then conduct a credit check on both the borrower and co-signer (if applicable).

If you are approved for the loan, the lender will send money directly to your school to pay for tuition and other education-related expenses.