Which Loan is Better: Subsidized or Unsubsidized?

If you’re looking for information on which type of loan is better for you, look no further! This blog post will cover the basics of subsidized and unsubsidized loans so that you can make an informed decision.

Checkout this video:

Subsidized Loans

A subsidized loan is a loan on which the interest is reduced by an explicit or hidden subsidy. The subsidy may be direct or indirect. Direct subsidies are paid by taxpayers to the lender, while indirect subsidies are absorbed by the borrower in the form of below-market rates.

The government pays the interest while the student is in school

The biggest advantage of a subsidized loan is that the government pays the interest while the student is in school. This means the student can focus on their studies and not have to worry about accruing interest on their loans. Once they graduate, they will then be responsible for paying off the loans, plus any interest that has accrued.

Subsidized loans are available to students who demonstrate financial need, as determined by the FAFSA. Not all students who are eligible for financial aid will qualify for a subsidized loan, as the amount of money available for these loans is limited. Students who do not receive a subsidized loan may be able to get an unsubsidized loan or another form of financial aid.

Students must demonstrate financial need

To be eligible for a Direct Subsidized Loan, you must be a U.S. citizen or eligible noncitizen, and you must demonstrate financial need. You also must be enrolled at least half-time in an eligible degree or certificate program at a school that participates in the Direct Loan Program.

Your school will determine the amount you can borrow, and the amount may not exceed your financial need. Also, the government pays the interest on a Direct Subsidized Loan while you’re in school at least half-time, for up to six months after you leave school (known as a grace period*), and during a deferment (a postponement of loan payments).

Students are not responsible for the interest that accrues while in school

Federal student loans offer two types of loans: subsidized and unsubsidized. Subsidized loans are need-based, meaning the government pays the interest that accrues while you’re in school. Unsubsidized loans are not need-based, so you are responsible for the interest that accrues while you’re in school.

The main difference between subsidized and unsubsidized loans is who is responsible for paying the interest while the borrower is in school. With a subsidized loan, the government pays the interest. With an unsubsidized loan, the borrower is responsible for paying the interest.

Subsidized loans are available to undergraduate students who demonstrate financial need. Unsubsidized loans are available to undergraduate and graduate students.

Unsubsidized Loans

The student is responsible for the interest that accrues while in school

If you have a subsidized loan, the government pays the interest while you’re in school. An unsubsidized loan means that you are responsible for the interest that accrues while in school. The biggest difference between subsidized and unsubsidized loans is that with a subsidized loan, you don’t have to pay the interest while you’re in school.

Students are not required to demonstrate financial need

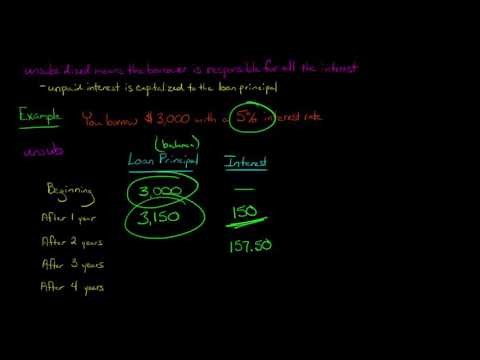

With an unsubsidized loan, students are not required to demonstrate financial need and the interest on the loan accrues while the student is in school. The borrower is responsible for all interest accrued. Repayment of principal and interest begins six months after graduation or when the borrower leaves school.

Students are responsible for the interest that accrues while in school

In order to avoid having the interest accrue while you are in school, you can either make interest payments while you are in school or capitalize the interest, which means that the interest will be added to the principal balance of your loan and will increase the amount you have to repay when you enter repayment.

Comparison

Subsidized loans are loans that are given to students who demonstrate financial need, as determined by the FAFSA. The government pays the interest on these loans while the student is enrolled in school at least half-time, during the grace period, and during deferment periods. Unsubsidized loans are not based on financial need; therefore, the borrower is responsible for paying the interest on the loan from the time the loan is disbursed until it is paid in full.

Subsidized loans have lower interest rates

The interest rate on a subsidized loan is lower than the interest rate on an unsubsidized loan because the government pays the interest while you are in school. You will have to begin repaying your loan six months after you leave school or drop below half-time enrollment. The repayment period is up to 10 years, depending on the amount you borrowed.

Unsubsidized loans are available to all students, regardless of financial need

Unsubsidized loans are available to all students, regardless of financial need. The interest on an unsubsidized loan accrues from the time the loan is disbursed and continues throughout the life of the loan. You can choose to pay the interest while you are in school and during grace periods and deferment or forbearance periods, or you can allow the interest to accrue and be capitalized (added to the unpaid principal balance of your loan).

Subsidized loans have a grace period before repayment begins

subsidized loans don’t start to accrue interest until after you graduate, whereas unsubsidized loans start to accrue interest as soon as you receive the loan.

Conclusion

After exploring the pros and cons of each type of loan, it is evident that neither loan is better than the other. It depends on the individual’s unique circumstances as to which loan would be the better choice. If the individual qualifies for a subsidized loan, then that would be the better choice because the interest is paid by the government while the student is in school. If the individual does not qualify for a subsidized loan, then an unsubsidized loan would be the better choice because the interest accrues while the student is in school, but it is not paid by the government.

Both types of loans have their pros and cons

There are two main types of student loans: subsidized and unsubsidized. Both have their pros and cons, so it’s important to understand the difference before you decide which one is right for you.

Subsidized loans are need-based, which means that they are awarded to students who demonstrate financial need. The government “subsidizes” these loans by paying the interest while the student is in school, during the grace period, and during any periods of deferment or forbearance.

Unsubsidized loans are not need-based, which means that they are available to any student, regardless of financial need. The borrower is responsible for paying the interest on these loans from the time they are disbursed until they are paid in full.

So, which type of loan is better? It depends on your individual circumstances. If you qualify for a subsidized loan and can get one, it’s probably your best option because you won’t have to pay any interest while you’re in school or during certain periods of deferment or forbearance. However, if you don’t qualify for a subsidized loan or can’t get one, an unsubsidized loan may be your only option. In this case, you should try to pay the interest while you’re in school so that it doesn’t accrue and increase your overall debt burden.

It is important to compare interest rates and repayment terms before deciding which loan is better for you

Student loans can be a necessary evil. They help you pay for school, but they also come with a hefty price tag. Interest rates, repayment terms, and other factors can make a big difference in the overall cost of your loan. That’s why it’s important to compare loans before you decide which one is right for you.

There are two main types of student loans: subsidized and unsubsidized. Subsidized loans are need-based, meaning that your financial need will be taken into account when your interest rate is calculated. Unsubsidized loans are not need-based, so your interest rate will be based solely on the market rate.

Subsidized loans also have the advantage of deferred interest. This means that the government will pay your interest while you are in school, during your grace period, and during any periods of deferment or forbearance. With an unsubsidized loan, you are responsible for all of the interest that accrues on your loan from the day that it is disbursed until it is paid in full.

So which type of loan is better? It depends on your individual circumstances. If you qualify for a subsidized loan, it may be a better option because of the lower interest rate and deferred interest feature. However, unsubsidized loans may be a better option if you do not qualify for a subsidized loan or if you need to borrow more money than the maximum amount allowed for a subsidized loan.

It’s important to compare all of the different factors involved in each type of loan before making a decision. Be sure to speak with a financial aid advisor to get more information about your options and to find out which type of loan would be best for you.