Which Best Explains What a Credit Score Represents?

Contents

A credit score is a numerical representation of your creditworthiness. It is based on your credit history, which is a record of your past borrowing and repayment behavior. The higher your score, the more likely you are to be approved for a loan or credit card and to get a favorable interest rate.

Checkout this video:

A credit score is a number that lenders use to decide whether to give you a loan and what interest rate to charge.

A credit score is a number that lenders use to decide whether to give you a loan and what interest rate to charge.

The higher your score, the better your chances of getting approved for a loan with a low interest rate. A lower score means you’re more likely to be denied a loan or get stuck with a higher rate.

A credit score is a statistical way to compare your credit risk with that of other borrowers.

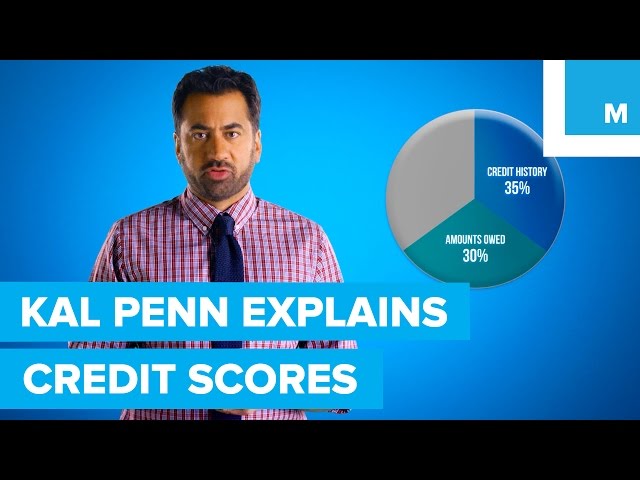

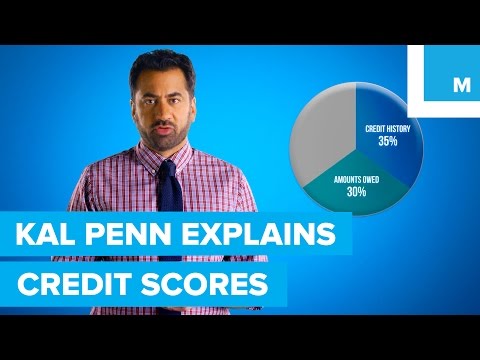

A credit score is a numerical expression based on a level analysis of a borrower’s credit files, to represent the creditworthiness of an individual. A credit score is primarily based on credit report information, typically from one of the three major credit bureaus: Experian, TransUnion, and Equifax. Income and employment history (or lack thereof) are not considered by the major credit bureaus when calculating credit scores.

Your lender or insurer may use a different FICO® Score than FICO® Score 8 or such other base or industry-specific FICO® Score, or another type of credit score altogether. Just remember that your credit score is often the same even if the number is not. For some consumers, however, the credit scores available may be different from FICO® Score 8. Based on their own internal scoring models, some lenders use scores that range from 300-850 while others use scores that range from 501-990 or somewhere in between.

A credit score is a snapshot of your credit history at a particular point in time.

A credit score is a number that creditors use to determine your creditworthiness. It is based on information in your credit report, and it helps lenders predict how likely you are to repay a loan. A high credit score indicates that you are a low-risk borrower, which means you are more likely to be approved for a loan with a lower interest rate.