What Percentage of Your Credit Card Limit Should You Use?

If you’re trying to keep your credit card usage low to improve your credit score, you might be wondering what percentage of your credit limit you should use. Here’s what you need to know.

Checkout this video:

Understanding Credit Utilization

Your credit utilization is the percentage of your credit card limit that you are currently using. For example, if your credit card limit is $1,000 and you have a balance of $500, your credit utilization is 50%. Generally, it’s best to keep your credit utilization below 30%. That’s because credit utilization is one of the factors that credit scoring models use to determine your credit score.

What is credit utilization?

Credit utilization is the second most important factor in your credit score—just behind payment history—and accounts for 30% of your total score.

Credit utilization is calculated by taking your total revolving credit (such as your credit card limits) and dividing that number by the amount of debt you currently carry on all revolvers. The lower your credit utilization, the better for your score—and vice versa.

For example, let’s say you have two credit cards: one with a $5,000 limit and another with a $10,000 limit. Your combined credit limit is $15,000. If you currently have a balance of $3,000 on both cards, your credit utilization would be 20%.

Why is credit utilization important?

Credit utilization is one of the primary indicators lenders look at when determining whether or not to extend youcredit and at what interest rate. A high utilization ratio signals to lenders that you might be overextended and more likely to miss payments or default on your loan—both of which would damage your score.

How can I lower my credit utilization?

There are two primary ways to lower your credit utilization ratio:

-Pay down your debt: The most obvious way to reduce your ratio is by paying down the balances on your revolving accounts. Even if you can’t pay off the entire balance, paying down as much as possible will help lower your ratio and improve your score.

-Increase your limit: If you have a good payment history with a particular lender, you can sometimes get them to increase your credit limit. This will immediately lower your ratio without affecting how much debt you actually owe.

How is credit utilization calculated?

Credit utilization is calculated by dividing your outstanding balance on revolving credit accounts by your total credit limit. For example, if you have a credit limit of $1,000 and a balance of $500, then your credit utilization is 50%.

Your credit utilization ratio is important because it is one of the factors that lenders look at when considering whether to approve you for a loan or extend you a line of credit. A high credit utilization ratio may indicate to lenders that you are overextended and may have difficulty making your payments on time.

There are two things you can do to improve your credit utilization ratio:

1) Pay down your outstanding balances. This will immediately reduce your credit utilization ratio.

2) Ask your lender to increase your credit limit. This will increase the denominator in the calculation, resulting in a lower credit utilization ratio.

What is a good credit utilization ratio?

Credit utilization is the amount of your credit limit that you use. For example, if your credit limit is $1,000 and you have a balance of $500, your credit utilization ratio is 50%. Credit utilization is important because it makes up 30% of your credit score.

Ideally, you should aim for a credit utilization ratio of 30% or less. This means that if your credit limit is $1,000, you should have a balance of $300 or less. Having a lower credit utilization ratio shows lenders that you’re a responsible borrower and helps improve your credit score.

The 30% Rule

What is the 30% rule?

The 30% rule is a general guideline that financial experts recommend to help people keep their credit card balances manageable. Essentially, the 30% rule says that you should never charge more than 30% of your credit card limit in a month. So, if your limit is $1,000, you would ideally only charge $300 or less in a given month.

There are a few reasons why the 30% rule is important. First, carrying a balance that makes up more than 30% of your credit limit can hurt your credit score. This is because credit utilization (i.e., the amount of debt you have compared to your available credit) is one factor that determines your credit score. So, if you’re trying to improve your credit score, it’s generally best to keep your utilization below 30%.

Second, carrying a large balance on your credit card can be expensive. This is because most cards have interest rates that range from about 15% to 25%. That means if you carry a balance of $300 (30% of a $1,000 limit), and your interest rate is 20%, you’ll end up paying about $60 in interest per year.

Of course, there may be times when you need to charge more than 30% of your credit limit in a month – for example, if you have an emergency expense or you’re making a large purchase. In these cases, it’s still important to try to pay off your balance as quickly as possible so you don’t end up paying too much in interest.

How does the 30% rule impact your credit score?

The 30% rule is a guideline often cited by financial experts that suggests you should use no more than 30% of your credit card limit at any given time. The logic behind this rule is that using too much of your credit limit can be a sign of financial instability, which can hurt your credit score.

There is some truth to this idea – using a high percentage of your credit limit can hurt your credit score. But the damage is not as severe as you might think, and there are other factors that have a much bigger impact on your score. In fact, following the 30% rule may actually do more harm than good.

Here’s what you need to know about the 30% rule and how it impacts your credit score.

First, it’s important to understand how your credit utilization ratio is calculated. This ratio is simply the amount of debt you have divided by the amount of credit you have available. So, if you have a $1,000 balance on a card with a $5,000 limit, your credit utilization ratio would be 20%.

Most experts agree that it’s best to keep your credit utilization ratio below 30%. In fact, many suggest keeping it below 10% for optimal results. But here’s the thing: the impact of your credit utilization ratio on your score starts to decrease once it hits 30%. So, if your utilization ratio is 31%, your score will only be marginally lower than it would be if your ratio was 29%.

This means that following the 30% rule may not have as big of an impact on your score as you think. And in some cases, it may actually do more harm than good.

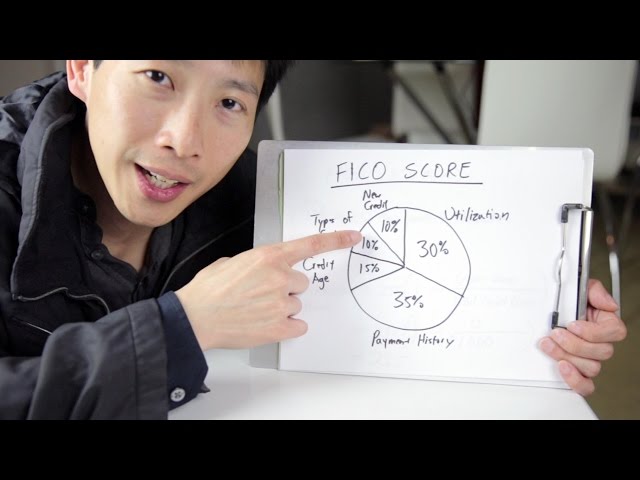

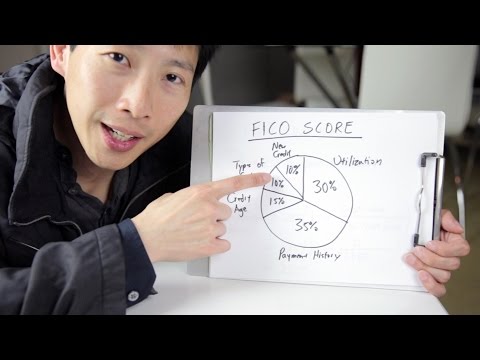

If you’re trying to improve your credit score, there are other things you should focus on first. For example, paying all of your bills on time – including utility bills, rent payments, and other types of accounts – will have a much bigger impact on your score than keeping your credit utilization below 30%. In fact, 35% of your FICO® Score is based on your payment history. So make sure that’s always a priority.

Are there exceptions to the 30% rule?

The 30% rule is generally a good guideline to follow, but there are a few exceptions. If you have a very high credit limit, for example, using 30% of your available credit may not have as big of an impact on your credit score as it would for someone with a lower credit limit. This is because the amount you owe makes up only 30% of your credit score—the rest is made up of your payment history (35%), length of credit history (15%), and credit mix (10%). So, if you have a long history of responsible credit use and a diverse mix of accounts, carrying a higher balance may not have as much of an effect on your score.

Another exception to the rule is if you’re trying to improve your credit utilization ratio in order to get a loan or qualify for a lower interest rate. In this case, you may want to use less than 30% of your available credit so that your ratio appears more favorable to lenders.

Finally, keep in mind that the 30% rule is meant to be used as a general guideline—if you’re carrying a balance that’s comfortable for you and aren’t worried about the impact on your credit score, there’s no need to strictly adhere to it.

Other Factors to Consider

While it’s important to keep your credit utilization low in order to improve your credit score, there are other factors that come into play as well. Your credit score is determined by a number of factors, including your payment history, credit history, and credit mix.

Your credit history

Your credit history is one of the most important factors in determining your credit score. Lenders want to see a history of on-time payments and responsible credit management. If you have a history of late payments or maxing out your credit cards, you will likely have a lower credit score.

Other factors that can impact your credit score include:

-The number of open accounts you have

-The length of your credit history

-The types of credit you have (revolving, installment, etc.)

-Recent credit activity (e.g., new accounts or hard inquiries)

Your credit card issuer

Credit utilization is one factor that makes up your credit score. The credit scoring formula looks at the amount of debt you have relative to your credit limit, and the more of your credit limit you use, the lower your score will be. So, if you want to keep your score high, it’s important to keep your credit utilization low.

But how low should it be? That’s a question with no definitive answer, but there are some general guidelines you can follow. One rule of thumb is to keep your utilization below 30%, but some experts say even 20% is too high.

Another factor to consider is your credit card issuer. Some issuers report your balance to the credit bureaus every month, even if you pay it in full. Others only report your balance if you carry a balance from one month to the next. If your issuer reports your balance every month, it’s important to keep your utilization low every month to avoid a potential drop in your score.

Your credit goals

There is no magic number when it comes to using your credit card, but there are a few things to consider when you are trying to decide what percentage of your credit limit you should use.

Your credit score is one factor that lending institutions look at when they are considering approving a loan or extending credit. The higher your credit score, the better your chances of getting approved for a loan with favorable terms.

If you are trying to improve your credit score, using a lower percentage of your credit limit can help. This is because one of the factors that is used to calculate your credit score is your credit utilization ratio, which is the amount of available credit you are using. So, if you have a $1000 credit limit and you use $500 of it, your credit utilization ratio is 50%. Using a lower percentage of your available credit can help improve your credit utilization ratio and, in turn, improve yourcredit score.

Another thing to consider when deciding how much of your credit limit to use is the interest rate you are paying on your outstanding balance. The higher the interest rate, the more it will cost you to carry a balance on your card from month to month. So, if you are paying a high interest rate on your outstanding balance, it may make sense to keep that balance as low as possible in order to minimize the amount of interest you pay each month.

Ultimately, there is no right or wrong answer when it comes to choosing what percentage of your credit limit to use. It depends on factors such as your personal financial situation and goals.