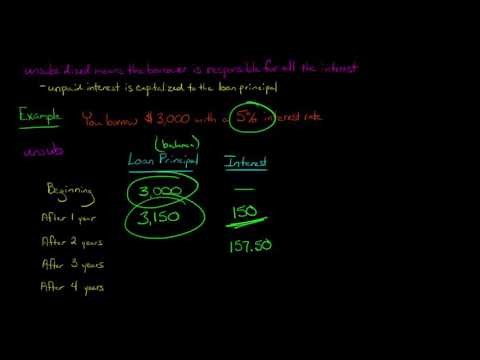

What is a Subsidized Loan for College?

Contents

A subsidized loan is a type of federal student aid that doesn’t accrue interest while you’re in school. If you qualify, the government will pay the interest on your loan while you’re in school and during your grace period.

Checkout this video:

Introduction

A subsidized loan is a need-based loan offered by the federal government to help students pay for college. The government pays the interest on these loans while the borrower is in school, during their grace period, and during any deferment periods.

Subsidized loans are available to undergraduate students who demonstrate financial need. The amount of the subsidy is based on the student’s financial need, as determined by the Free Application for Federal Student Aid (FAFSA).

The maximum amount that a student can borrow in a subsidized loan depends on their year in school and other financial aid they are receiving. For example, first-year undergraduate students can borrow up to $3,500 in a subsidized loan. The maximum amount increases each year, up to $5,500 for third-year and beyond undergraduates.

There are two types of subsidized loans: Direct Subsidized Loans and Federal Perkins Loans. Direct Subsidized Loans are available to undergraduate and graduate students with financial need. Federal Perkins Loans are only available to undergraduate and graduate students with exceptional financial need.

Subsidized loans have fixed interest rates that are set by Congress each year. For Direct Subsidized Loans first disbursed on or after July 1, 2019, and before July 1, 2020, the interest rate is 4.53%. For Federal Perkins Loans first disbursed on or after October 1, 2019, and before October 1, 2020, the interest rate is 5%.

What is a Subsidized Loan?

A subsidized loan is a need-based loan awarded by the government to help students pay for college. If you qualify, the government will pay the interest on your loan while you’re in school. These loans are typically offered at a lower interest rate than unsubsidized loans. You may also be eligible for a subsidized loan if you’re in an economic hardship or other qualifying situation.

How Do Subsidized Loans Work?

A subsidized loan is a type of financial aid that is awarded based on need. The U.S. Department of Education pays the interest on subsidized loans while the student is in school at least half-time, during their grace period, and during deferment periods.

To be eligible for a subsidized loan, students must demonstrate financial need as determined by their Free Application for Federal Student Aid (FAFSA). Only undergraduates are eligible for subsidized loans.

The interest rate on a subsidized loan is fixed and generally lower than the rates on unsubsidized loans and private loans. The amount students can borrow each year in subsidized loans is capped by law. The maximum amount that can be borrowed depends on the student’s year in school and whether they are dependent or independent.

Who is Eligible for a Subsidized Loan?

To be eligible for a subsidized loan, you must:

– Demonstrate financial need

– Be enrolled at least half-time in an eligible program

– Be a U.S. citizen or eligible non-citizen

– Not be in default on any federal student loans

– Not have reached your limit on subsidized loan borrowing

What are the Benefits of a Subsidized Loan?

Federal subsidized loans are available to undergraduate students who demonstrate financial need. The need is determined by the information provided on the Free Application for Federal Student Aid (FAFSA®) form.

A key benefit of a subsidies loan is that the federal government pays the interest while the student is in college, during the six-month grace period after graduation, and during any deferment periods. This can save the borrower a significant amount of money over time.

Another benefit of subsidized loans is that they have fixed interest rates that are lower than the rates on unsubsidized loans and most private loans. The interest rate for subsidized loans first disbursed on or after July 1, 2020, and before July 1, 2021, is 2.75%.

Subsidized loans also come with more flexible repayment options than unsubsidized loans. For example, borrowers can choose to make payments based on their income with an income-driven repayment plan.

To learn more about subsidized loans, visit StudentAid.gov/subsidized-loans.

What are the Disadvantages of a Subsidized Loan?

There are some potential disadvantages to taking out a subsidized loan for college. One is that you may not be able to borrow as much money as you could with an unsubsidized loan. Another is that you may have to pay a origination fee, which is a percentage of the total loan amount that is deducted from the loan before it is disbursed to you. Finally, if you default on your loan, your school could withhold your diploma until the debt is repaid.

Conclusion

Assuming you qualify for a subsidized loan, you may wonder whether it’s worth taking out this type of loan over an unsubsidized or Perkins Loan. Subsidized loans definitely have their advantages — the low interest rate and deferment options make them a good choice for many borrowers. However, keep in mind that you will have to repay your loans, with interest, after you graduate or leave school. Make sure you understand all of your options before you take out any type of loan.