What is a Minimum Payment on a Credit Card?

Contents

If you have a credit card, you probably know that you have to make a minimum payment each month. But what is a minimum payment, and how is it calculated? We’ve got the answers.

Checkout this video:

Minimum Payments

What is a minimum payment?

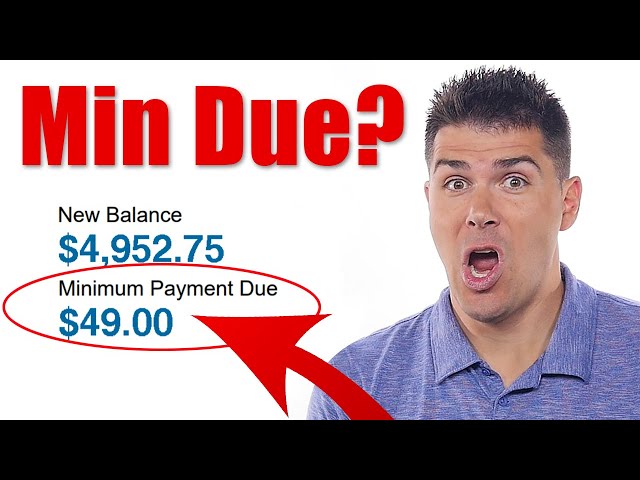

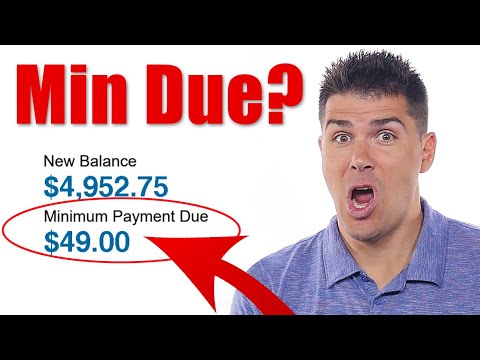

A minimum payment is the smallest amount of money that you can pay on your credit card bill each month. Credit card companies set minimum payments as a percentage of your total balance, usually between 2% and 4%. So, if your credit card balance is $1,000 and your minimum payment is 3%, you would owe at least $30.

Minimum payments are designed to keep you indebted to your credit card company for as long as possible. The longer it takes you to pay off your credit card debt, the more interest you will pay. For this reason, it’s always best to pay more than the minimum payment each month.

If you only make the minimum payment on a credit card with a $1,000 balance and an 18% annual interest rate, it would take you more than 25 years to pay off the debt. And, you would end up paying more than $5,000 in interest!

How is a minimum payment calculated?

Your minimum payment is calculated as a percentage of your outstanding balance, or as a flat dollar amount, whichever is greater. The percentage is usually between 1 and 3 percent, and the flat dollar amount is typically $25. So, if you have a balance of $1,000 and your minimum payment is calculated as 3 percent, your minimum amount due would be $30. If your minimum payment was calculated as a flat dollar amount and it was $25, your minimum amount due would also be $25.

Your credit card issuer must disclose the method used to calculate your minimum payment on your monthly statement.

Pros and Cons of Making a Minimum Payment

If you have a high interest rate on your credit card, making only the minimum payment each month could cost you a lot of money in interest charges. On the other hand, if you are in a tight spot financially, making the minimum payment might be all you can afford. Let’s look at the pros and cons of making a minimum payment on your credit card.

Pros

There are a few potential benefits to making a minimum payment on your credit card. First, it can help you avoid late fees and penalties. If you’re struggling to make ends meet, making a lower payment can help you keep your account in good standing. Additionally, some credit card companies may report your payments to the credit bureaus even if you only make the minimum payment. This could help you improve your credit score over time.

##Heading: Cons

##Expansion:

There are also some potential downside to making a minimum payment on your credit card. First, it will take much longer to pay off your balance if you only make the minimum payment each month. Additionally, the interest charges on your account will continue to add up, costing you more money in the long run. Finally, making only the minimum payment may negatively impact your credit score if your credit card company reports this information to the credit bureaus.

Cons

minimum payment is often just a small percentage of your outstanding balance, which means you’ll be paying off your debt for a long time.

Paying only the minimum also means you’ll be paying a lot of interest.

Minimum payments can also hurt your credit score by lengthening your credit utilization ratio—the amount of debt you have compared to your credit limit.

This is because it indicates to creditors that you’re only able to make small payments and may not be able to pay back what you owe in full.

Should You Make a Minimum Payment?

The minimum payment on a credit card is the lowest amount of money you can pay on your credit card bill without being charged a late fee. Most credit card companies require a minimum payment of two percent of your balance, or $15, whichever is greater. So, if your balance is $100, you would need to pay at least $2.

When it makes sense to make a minimum payment

If your goal is simply to avoid getting penalized with a late fee or increased interest rate, then making a minimum payment might suffice. However, if you want to actually get ahead on your debt, you need to do more than just make the minimum payment.

For starters, minimum payments are generally calculated as a small percentage of your balance, plus any interest and fees that have accrued. This means that if you only make the minimum payment each month, it will take you much longer to pay off your debt because you’re not chipping away at the principal.

Minimum payments also do nothing to improve your credit score. In fact, making only the minimum payment can actually hurt your score because it shows that you’re not keeping up with your debt obligations. If you’re trying to improve your credit score so you can qualify for a loan or get a better interest rate, making the minimum payment is not going to help.

If you can’t afford to do any more than the minimum payment each month, that’s not necessarily a bad thing. Just be aware that it will take longer to get out of debt and that it could have an impact on your credit score. If you’re able to make more than the minimum payment each month, do it! Even an extra $50 per month can make a big difference in the long run.

When it doesn’t make sense to make a minimum payment

If you’re already struggling to make ends meet, paying only the minimum on your credit card debt will likely make things worse. That’s because the minimum payment is typically just a small percentage of your overall balance, plus any fees and interest charges. As a result, it can take years — even decades — to pay off your debt if you only make minimum payments.

What’s more, making only minimum payments can cost you a fortune in interest charges. Credit card companies typically assess interest on your outstanding balance every month. So, even if you pay off part of your balance each month, you’ll still be charged interest on the unpaid portion.

In some cases, it might make sense to pay only the minimum. For example, if you have a low interest rate and you can afford to pay more than the minimum each month, you may want to do that to avoid accruing too much interest. But in most cases, it’s best to try to pay off your credit card debt as quickly as possible.

How to Avoid Making a Minimum Payment

A minimum payment is the smallest amount of money that you can pay on your credit card bill each month. The minimum payment is usually a percentage of your total balance, and it’s typically around 2%. For example, if your credit card balance is $1,000, your minimum payment would be $20.

Tips for avoiding minimum payments

One of the worst things you can do with your credit card is only make the minimum payment each month. By only paying the minimum, you’ll end up paying more in interest and it will take you much longer to pay off your debt. If you’re struggling to make more than the minimum payment, here are a few tips to help you out:

-Create a budget and stick to it. Knowing where your money is going each month will help you free up some extra cash to put towards your credit card debt.

-Consider transferring your balance to a low interest credit card. This can help you save on interest and pay off your debt faster.

-Make extra payments when you can. Every little bit helps!

-Talk to your credit card company. They may be able to work with you to create a payment plan or lower your interest rate.

What to Do if You Can’t Avoid Making a Minimum Payment

The Credit CARD Act of 2009 requires credit card companies to give 45 days notice before making any changes to interest rates, fees, and other terms. This includes changing the minimum payment amount. So, if you receive a notice that your minimum payment is going up, you’ll have some time to adjust your budget accordingly. But what if you can’t make the new minimum payment?

What to do if you can’t avoid making a minimum payment

If you find yourself in a situation where you can’t avoid making a minimum payment on your credit card, there are a few things you can do to ease the financial burden. One option is to call your credit card company and ask for a lower interest rate. This could help you save money on interest charges and make it easier to pay off your balance. You could also ask for a grace period, which would give you extra time to pay off your balance without accruing interest. Finally, you could try to negotiate a lower monthly payment with your credit card company. If you are unable to do any of these things, you may need to consider other options, such as transferring your balance to a lower-interest credit card or taking out a personal loan.