What is a Car Loan?

Contents

A car loan is a loan that helps you finance the purchase of a vehicle. You can get a car loan through a bank, credit union, or other financial institution. The loan is secured by the car itself, which means that if you default on the loan, the lender can repossess the car.

Checkout this video:

Introduction

A car loan is a type of loan that is used to finance the purchase of a car. It is usually repaid over a period of time, known as the term of the loan, and typically has a fixed interest rate.

Car loans can be used to finance the purchase of both new and used cars, and can be obtained from a range of different lenders, including banks, credit unions, and specialist lenders.

The amount that can be borrowed, the interest rate charged, and the term of the loan will all vary depending on the lender and the borrower’s individual circumstances.

How do car loans work?

A car loan is a type of loan used to finance the purchase of a vehicle. Car loans are typically made by banks or credit unions and are paid back over a set period of time, usually two to five years. The interest rate on a car loan is typically lower than the interest rate on a credit card or personal loan. When you take out a car loan, you agree to pay back the loan plus interest.

The basics of car loans

A car loan is a type of personal loan that you can use to finance the purchase of a new or used car. Car loans are available from a variety of lenders, including banks, credit unions, and online lenders.

The terms of a car loan will vary depending on the lender, but usually include a repayment period of two to seven years. Interest rates on car loans are typically lower than rates on other types of loans, such as personal loans or credit cards.

When you take out a car loan, you will need to provide the lender with some information about yourself and your finances. This includes your credit score, employment history, and income. The lender will use this information to decide whether or not to approve your loan and what interest rate to charge.

Once you have been approved for a loan, you will need to choose a vehicle and negotiate a price with the seller. Once the price has been agreed upon, the lender will provide you with the funds needed to purchase the vehicle. You will then make monthly payments on the loan until it is paid off in full.

How to get a car loan

You can get a car loan from a bank, credit union, online lender or dealership.

Banks, credit unions and online lenders offer loans to customers with good to excellent credit. Dealerships offer financing through their own lending sources or banks and credit unions.

To get the best interest rate on a loan, you need to have good to excellent credit. The higher your credit score, the lower the interest rate you’ll qualify for.

When you apply for a loan, the lender will pull your credit report and score. They will use this information to determine whether you qualify for a loan and what interest rate they can offer you.

If you have good to excellent credit, you’ll likely qualify for a competitive interest rate on a loan. If you have poor credit, you may still be able to get a loan but you’ll likely pay a higher interest rate.

Types of car loans

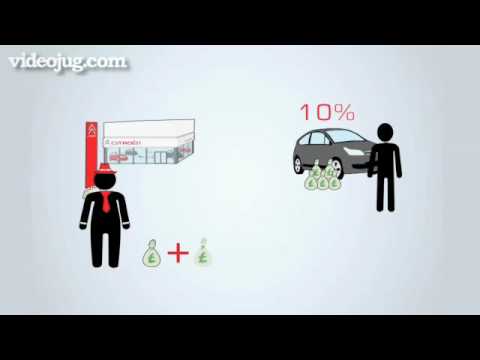

There are several types of car loans available to consumers. The most popular type of loan is the bank loan, which is usually the cheapest option. There are also finance companies that specialise in car loans, and these can be a good option if you have a poor credit history. There are also some specialist lenders who offer car loans to people with poor credit histories.

Secured car loans

A secured car loan is a loan that uses your car as security for the loan. This means that if you default on the loan, your car can be repossessed.

Secured car loans are often used by people who have a poor credit history, as they offer a lower risk to the lender. However, this means that they usually come with a higher interest rate than unsecured loans.

If you are considering a secured loan, make sure you are aware of the risks involved before signing any agreements.

Unsecured car loans

An unsecured car loan is a loan that is not backed by any collateral, such as a vehicle. Unsecured car loans are riskier for lenders because there is no asset to repossess if you default on the loan. As a result, unsecured car loans typically have higher interest rates than secured loans.

Unsecured car loans are available from some banks, credit unions, and online lenders. The eligibility requirements and terms of unsecured car loans vary depending on the lender.

To qualify for an unsecured car loan, you will likely need good credit and a steady income. Some lenders may also require you to have a cosigner who agrees to be responsible for the loan if you default.

Pros and cons of car loans

A car loan is a loan that is taken out to purchase a car. The loan is typically paid back over a period of time, usually two to five years. Car loans typically have lower interest rates than other types of loans, such as personal loans. However, there are some drawbacks to car loans.

Pros of car loans

A car loan can help you to buy the car of your dreams without having to pay the full amount upfront. This means that you can drive away in your new car sooner than if you were to save up the entire purchase price.

Car loans also give you the opportunity to build your credit history, which can be helpful if you need to take out other types of loans in the future (e.g., a mortgage).

Finally, car loans typically have relatively low interest rates, which means that your monthly payments will be affordable.

Cons of car loans

While car loans can offer a number of advantages, there are also some potential disadvantages to consider. One of the biggest potential drawbacks of taking out a car loan is that you may end up paying more for your car than you would if you paid in cash. This is because loan providers typically charge interest on the money that you borrow, which can add up over time.

Another potential downside of car loans is that they can put a strain on your finances, particularly if you have other debts to pay off at the same time. When you take out a loan, you will be required to make regular repayments, which can leave you with less money each month to cover other essential costs such as food and rent. If you miss any loan repayments, this could also damage your credit score, making it more difficult to borrow money in the future.

How to compare car loans

When you’re looking to finance a car, it’s important to compare car loans to get the best deal. By understanding the difference between secured and unsecured car loans, as well as the different interest rates and repayment options available, you can make sure you choose the right loan for your needs.

Interest rates

The interest rate on a car loan is the cost of borrowing money from a lending institution expressed as a percentage of the loan amount. Interest rates are usually fixed, which means they do not change over the life of the loan, or variable, which means they can go up or down during the life of the loan. The interest rate you pay will affect the total cost of your loan.

Loan terms

The loan term is the length of time you have to repay your loan. Loan terms can range from 12 to 84 months, but the average car loan term is around 60 months.

Shorter loan terms usually mean higher monthly payments, but they also mean that you’ll pay less in interest over the life of the loan. Longer loan terms mean lower monthly payments, but you’ll pay more in interest over time.

The best way to decide what loan term is best for you is to compare your monthly budget with the total amount of interest you’ll pay over the life of the loan. If you can afford the higher monthly payments of a shorter loan, you’ll save money in the long run. If you need lower monthly payments, a longer loan term might be a better option.

Fees and charges

When you compare car loans, make sure you’re aware of all the fees and charges that might apply. These can include:

-Application fees: Some lenders charge a fee just to apply for a loan. This is usually a flat fee, but in some cases it can be a percentage of the loan amount.

-Valuation fees: If you’re borrowing money to buy a car, the lender will usually want to value the car to make sure it’s worth at least as much as the amount you’re borrowing. This fee is usually around $100.

-Monthly account-keeping fees: Many lenders charge a small monthly fee to cover the cost of maintaining your account. This is usually around $5 per month.

-Early repayment fees: If you pay off your loan early, some lenders will charge a fee. This is sometimes called a ‘break costs’ or ‘exit fees’. It’s important to check for early repayment fees before taking out a loan, so that you know how much it will cost if you want to pay off your loan early.

FAQs

A car loan is a loan that helps you finance the purchase of a vehicle. It’s usually for a period of 36 to 60 months, and you’ll make fixed payments during that time. You’ll need to have good credit to qualify for a car loan.

What is the difference between a car loan and a personal loan?

Car loans and personal loans are both types of installment loans, which means they are loans that are paid back in monthly payments. However, there are some key differences between the two.

Car loans are specifically for the purchase of a car, and the car is used as collateral for the loan. This means that if you default on the loan, the lender can repossess the car. Personal loans can be used for a variety of purposes, including buying a car, but they are not secured by any collateral. This makes personal loans a higher risk for lenders, and as a result, personal loan interest rates are usually higher than car loan interest rates.

Can I get a car loan with bad credit?

Many people worry that they won’t be able to get a car loan because of their bad credit. The good news is that there are options available for people with bad credit. You can either work with a subprime lender or a traditional lender that offers special financing for people with bad credit. There are also a few things you can do to improve your chances of getting approved for a loan, such as saving up for a larger down payment or cosigning the loan with a friend or family member.

How can I get the best car loan interest rate?

The lowest car loan interest rates are reserved for borrowers with the best credit scores. Rates can vary significantly from one lender to the next, so it pays to shop around for the best deal. Borrowers with spotless credit profiles should have no problem qualifying for the lowest advertised rates.

Those with less-than-perfect credit may still be able to get a low rate, but they may need to do some comparison shopping to find the best deal. It’s also important to remember that the interest rate is only one factor in the overall cost of a car loan. Borrowers should compare total costs, including fees, before choosing a lender.

Conclusion

In conclusion, a car loan is a type of loan that is used to finance the purchase of a vehicle. The loan is typically repaid over a period of time, and the borrower may be required to make periodic payments toward the loan principal and interest. Car loans may be available from banks, credit unions, and other financial institutions, and the terms of the loan may vary depending on the lender.