What Does an Unsubsidized Loan Mean?

Contents

You may have heard the term “unsubsidized loan” before but what does it actually mean? In this blog post, we’ll explain everything you need to know about unsubsidized loans .

Checkout this video:

Introduction

An unsubsidized loan is a type of financial aid that you have to repay with interest. The U.S. Department of Education offers these loans to eligible undergraduate and graduate students, but you’re responsible for paying the interest even while you’re in school and during your grace period.

What is an Unsubsidized Loan?

An unsubsidized loan is a type of financial aid that you have to pay back. The main difference between subsidized and unsubsidized loans is that with a subsidized loan, the government pays the interest while you’re in school. With an unsubsidized loan, you are responsible for paying the interest from the day the loan is disbursed until it is paid in full.

If you choose not to pay the interest while you’re in school, it will be added to the principal amount of your loan (known as “capitalization”), and your monthly payments will be higher and it will take you longer to pay off the loan.

How Unsubsidized Loans Work

Unsubsidized loans are federal student loans available to undergraduate, graduate, and professional degree students. The US Department of Education (ED) is the lender. You’re not required to demonstrate financial need to receive an unsubsidized loan.

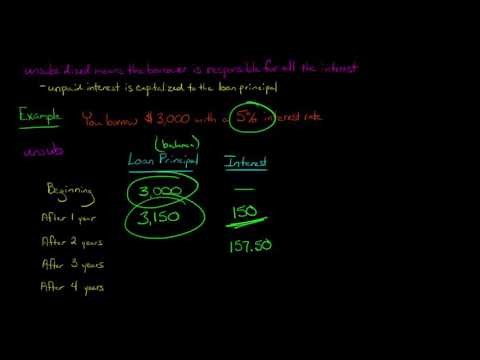

With unsubsidized loans, interest accrues from the time the loan is disbursed until it’s paid in full. If you choose not to pay the interest while you’re in school and during certain periods of deferment or forbearance, your interest will capitalize (accumulate) and be added to the principal balance of your loan. This will increase the amount you have to repay.

Advantages of Unsubsidized Loans

There are a few advantages to taking out an unsubsidized loan:

-You’re not required to demonstrate financial need in order to qualify for the loan.

-The interest on your loan begins accruing immediately, but you don’t have to make any payments until after you graduate (or leave school).

-You can choose to make interest-only payments while you’re in school, which can help keep your loan balance from growing too large.

Disadvantages of Unsubsidized Loans

The main disadvantage of an unsubsidized loan is that the borrower is responsible for all the interest that accrues on the loan from the date of disbursement. This can add a significant amount to the total cost of the loan over time.

Conclusion

In conclusion, an unsubsidized loan is a loan that is not backed by the government. This means that the interest on the loan will accrue while you are in school and you will be responsible for paying it back once you enter repayment. These loans are typically more expensive than subsidized loans, but they can still be a good option for financing your education.