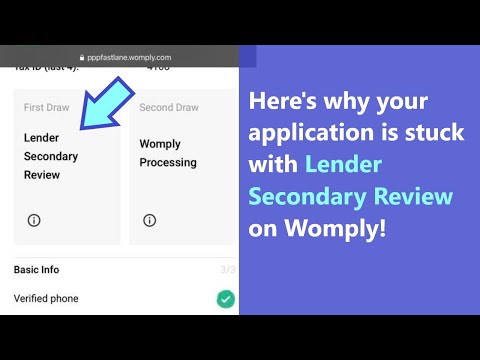

What Does ‘Lender Secondary Review’ Mean on a PPP Loan?

Contents

If you’re a small business owner who has applied for a Paycheck Protection Program (PPP) loan, you may have come across the term “lender secondary review.” But what does this mean, and why is it important?

Checkout this video:

What is the ‘Lender Secondary Review’?

The ‘lender secondary review’ is a process that some lenders use to verify the information that you submitted on your Paycheck Protection Program (PPP) loan application. This review is usually done after the SBA has approved your loan.

What is the purpose of the ‘Lender Secondary Review’?

The ‘Lender Secondary Review’ is a process that lenders use to review Paycheck Protection Program (PPP) loan applications that have been approved by the Small Business Administration (SBA).

The purpose of the ‘Lender Secondary Review’ is to ensure that the borrower meets all of the eligibility requirements for the PPP loan and that the loan amount requested is accurate.

If the lender finds that the borrower does not meet all of the eligibility requirements or that the loan amount requested is not accurate, the lender may choose to deny the loan or reduce the loan amount.

What does the ‘Lender Secondary Review’ process entail?

The ‘Lender Secondary Review’ is the term used to describe the process that lenders must go through in order to receive full forgiveness for their Paycheck Protection Program (PPP) loans.

In order to receive full forgiveness, lenders must first submit an application to the Small Business Administration (SBA). This application must include documentation demonstrating that the loan was used for its intended purpose, which is to support payroll and other eligible expenses.

Once the SBA has received and reviewed the application, they will determine whether or not the loan is eligible for full forgiveness. If the SBA determines that the loan is eligible for full forgiveness, they will then notify the lender and instruct them to begin making payments on the loan. If the SBA determines that the loan is not eligible for full forgiveness, they will notify the lender and instruct them to begin making payments on the unpaid portion of the loan.

Who is eligible for the ‘Lender Secondary Review’?

The ‘Lender Secondary Review’ is a process that is required for all Paycheck Protection Program (PPP) loans. Any business that has applied for a PPP loan must go through this review process. The ‘Lender Secondary Review’ is designed to ensure that all PPP loan requirements have been met by the business and that the loan is not at risk of default.

What are the eligibility requirements for the ‘Lender Secondary Review’?

To be eligible for the ‘Lender Secondary Review’, your business must:

-Have 300 or fewer employees

-Have a physical location in the US

-Befor-profit

-Have used or will use the loan proceeds for eligible expenses, as outlined in the CARES Act

How does the ‘Lender Secondary Review’ process work?

If your small business applied for and was approved for a Paycheck Protection Program (PPP) loan, your lender will likely conduct a “lender secondary review” after the SBA has reviewed and approved your loan forgiveness application.

What is the ‘Lender Secondary Review’ process?

The ‘Lender Secondary Review’ process is when the Small Business Administration (SBA) reviews your Paycheck Protection Program (PPP) application after your lender has already approved it.

The SBA will look at things like whether you truly need the loan and if you will be able to meet the requirements for forgiveness.

If the SBA approves your loan, they will send you a notice of their decision. If they deny your loan, they will send you a notice of their decision and explain why your loan was denied.

How long does the ‘Lender Secondary Review’ process take?

The “lender secondary review” is the final stage of the Paycheck Protection Program loan application process. After your application is approved by the Small Business Administration, it will be sent to your lender for a final review.

This review usually takes place within 1-2 weeks, and during this time your lender will verify your eligibility and confirm that you have provided all of the required documentation. Once your lender has completed the secondary review, they will issue you a promissory note and your loan will be disbursed.

What are the benefits of the ‘Lender Secondary Review’?

The ‘Lender Secondary Review’ is a process that is required for all Paycheck Protection Program (PPP) loan applications. This review is conducted by the lender after the Small Business Administration (SBA) has completed their initial review of the application. The lender will review the information provided by the borrower and determine if the borrower is eligible for the loan.

What are the benefits of the ‘Lender Secondary Review’ process?

The ‘Lender Secondary Review’ process is when a PPP loan is reviewed by the lender after the borrower has submitted their application. This allows the lender to verify information and ensure that the borrower meets all eligibility requirements. This helps to protect both the borrower and the lender, and ensures that only qualified borrowers receive a PPP loan.