How to Purchase a Home with Bad Credit

Contents

It is possible to purchase a home with bad credit. Follow these steps to improve your credit score and get into the home of your dreams.

Checkout this video:

Check your credit score

If you have bad credit, the first thing you should do is check your credit score. You can get a free copy of your credit report from each of the three major credit bureaus — Equifax, Experian and TransUnion — once a year at AnnualCreditReport.com. Reviewing your credit report will give you an idea of where your score stands and help you identify any errors that could be dragging it down.

If you find any errors, dispute them with the credit bureau using the information on their website. Once the error is corrected, your score should go up. If you don’t find any errors, there are still a few things you can do to improve your score.

Get pre-approved for a mortgage

If you have bad credit, the first step in purchasing a home is to get pre-approved for a mortgage. To do this, you’ll need to provide your lender with some basic information about your financial history, including your employment history, income, debts and any assets you may have.

Lenders will use this information to determine whether or not you qualify for a loan and, if so, how much they’re willing to lend you. Getting pre-approved for a mortgage is the first step in the home-buying process and can make it easier to find a home that’s within your budget.

Once you’ve been pre-approved for a loan, you can start shopping for a home. When you find a home that you want to purchase, your lender will order an appraisal to make sure that the home is worth the amount they’re willing to lend. If the appraisal comes back lower than the purchase price, you may need to negotiate with the seller to lower the price of the home.

If everything goes smoothly, you should be able to close on your new home within 30-60 days after finding it.

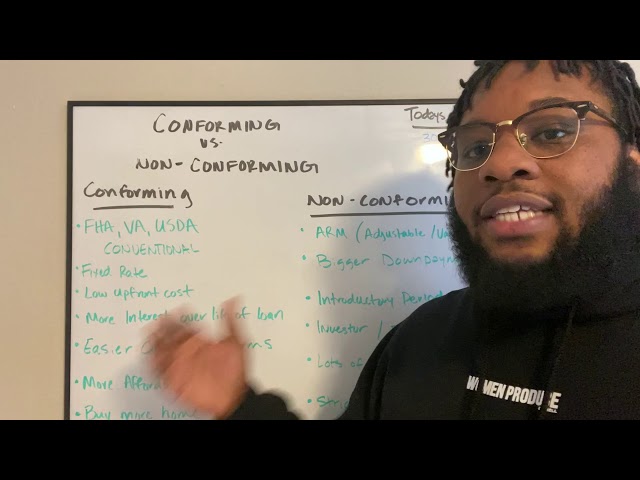

Look for a government-backed loan

The first step to buying a home with bad credit is to look for a government-backed loan. These loans are backed by the U.S. Department of Housing and Urban Development (HUD) or the Federal Housing Administration (FHA). They are designed for people with low credit scores and are more forgiving when it comes to things like bankruptcies and foreclosures.

There are two types of government-backed loans: FHA loans and VA loans. FHA loans are available to anyone with a credit score of 580 or higher. If you have a credit score lower than 580, you may still be eligible for an FHA loan, but you will need to put down 10% as a down payment. VA loans are available only to veterans, active duty service members, and their spouses.

Find a cosigner

If you have bad credit, one of the best ways to get approved for a home loan is to find a cosigner with good credit. A cosigner is someone who agrees to be responsible for the loan if you default on it. This means that the lender will look at the cosigner’s credit history and income when deciding whether or not to approve the loan.

If you have a relative or friend who is willing to cosign for you, this can be a great option. Just make sure that you choose someone who has good credit and a steady income, as this will increase your chances of getting approved for the loan.

Get a loan from a private lender

If you have bad credit, your options for securing a loan are somewhat limited. However, you may still be able to get a loan from a private lender. Private lenders are typically individuals or small businesses, as opposed to large banks or financial institutions.

If you decide to go this route, be sure to do your research and choose a reputable lender. You should also be prepared to pay a higher interest rate than you would with a traditional loan, as private lenders often charge higher rates to offset the risk of lending to someone with bad credit.

Once you’ve found a lender, you’ll need to fill out an application and provide documentation of your income and expenses. If approved, you’ll then need to sign a loan agreement and make payments according to the terms of the loan.