How to Figure Interest on a Car Loan

Contents

Find out how to figure interest on a car loan so you can be prepared when it comes time to make your payment.

Checkout this video:

How to Figure Interest on a Car Loan

The interest rate on a car loan is the cost of borrowing money from the lender. It is expressed as a percentage of the loan amount and is computed for a specific period of time. The interest rate on a car loan is determined by several factors, including the vehicle’s purchase price, the loan amount, the length of the loan, and the borrower’s credit history.

Decide the loan amount

The first step is to decide how much you need to borrow. This is the principal loan amount and it’s what you’ll be making payments on. You’ll also need to decide the length of the loan, which is typically 36, 48, or 60 months. The longer the loan, the lower your monthly payment will be, but the higher the total interest you’ll pay over the life of the loan.

Decide the interest rate

The interest rate is the fee charged by the lender to the borrower for the use of money. In general, the higher the risk to the lender, the higher the interest rate. With a car loan, your credit score is one factor that determines the interest rate you’ll pay. Auto loan rates also vary depending on the type of vehicle you’re buying. Newer cars usually have lower interest rates than older cars.

There are a few other things that affect your car loan’s interest rate:

-The length of your loan: in general, shorter loans have lower interest rates than longer loans

-The amount of money you’re borrowing: in general, larger loans have higher interest rates than smaller loans

Decide the length of the loan in months

The length of the loan will play a role in how much interest you end up paying. To calculate your monthly payments, you’ll need to know the length of your loan in months. You can use an online calculator to figure out the monthly payment for different loan lengths, or you can use a simple formula. The formula is M = L[i(1 + i)n]/[(1 + i)n – 1], where M is the monthly payment, L is the loan amount, i is the interest rate per month, and n is the number of payments.

How to Use an Online Loan Calculator

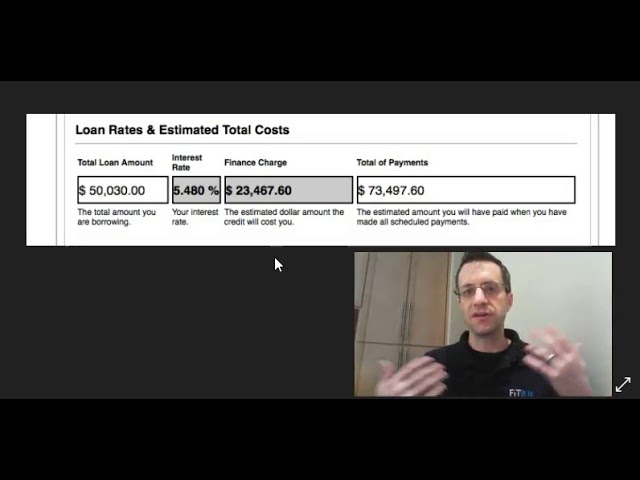

auto loan interest can add thousands of dollars to the price of a car. It’s important to know how to calculate interest on a car loan so that you can make an informed decision about your purchase. You can use an online loan calculator to figure out the interest on your car loan. Here’s how.

Find an online loan calculator

Calculating the interest on a car loan is a simple task that even those with no previous experience can handle. The first step is to find an online loan calculator. You can usually find one by searching for “online loan calculator” in your favorite search engine.

Once you have found a calculator, you will need to enter some information about your loan. The most important piece of information is the apr, or annual percentage rate. This is the interest rate that will be applied to your loan. You can usually find this information on your loan paperwork.

Next, you will need to enter the length of your loan in months. Most car loans are for either 36 or 60 months, but some loans may be for 72 or 84 months.

Finally, you will need to enter the amount of money you are borrowing. This is the total amount of money you will need to pay back, including interest.

After you have entered all of this information, the online calculator will figure out your monthly payment and the total amount of interest you will pay over the life of your loan.

Enter the loan amount

You can use an online loan calculator to figure out your monthly car loan payment, as well as the total interest you will pay on the loan. To use the calculator, you will need to know the loan amount, the interest rate, and the term of the loan.

Enter the loan amount into the calculator. This is the total amount that you will be borrowing from the lender.

Next, enter the interest rate into the calculator. The interest rate is the percentage of the loan that you will be charged in interest.

Finally, enter the term of the loan into the calculator. The term is the length of time that you have to repay the loan.

The calculator will then give you your monthly payment amount, as well as your total interest payments for the life of the loan.

Enter the interest rate

You’ll need to enter the interest rate you’re being offered on your car loan. This is a percentage, so if you’re being offered an interest rate of 6%, you’ll enter 6 into the calculator.

Enter the length of the loan in months

Once you have chosen the type of loan, you need to enter the loan amount, the interest rate, and the length of the loan in months. The interest rate is the percentage of the loan charged by the lender for borrowing the money. The length of the loan is how long you have to pay back the loan, which is typically between 36 and 60 months.

To calculate your monthly payment, you will need to enter your loan information into an online calculator. You can find several different kinds of calculators online by searching for “loan calculator.”

Once you have found a calculator that you like, enter in the following information:

-The loan amount

-The interest rate

-The length of the loan in months

-Your down payment (if you have one)

-The trade-in value of your car (if you have one)

After you have input all of the relevant information into the online loan calculator, click on the “Calculate” button. This will generate a report that includes your monthly payment amount, the interest rate, the total amount of interest you will pay over the life of the loan, and the total amount of the loan. The report will also show you a breakdown of how much interest you will pay each month.

How to Use the Formula to Figure Interest on a Car Loan

You can use a formula to figure interest on a car loan. The formula is I=P*r*t. You will need to know the loan’s principle, the interest rate, and the loan’s term to use the formula. The principle is the amount of money you borrowed. The interest rate is the percentage of the loan that you will pay in interest. The loan’s term is the amount of time you have to pay back the loan.

Determine the periodic interest rate

Most car loans are amortized over a period of time, with fixed payments. You can use a simple formula to determine the periodic interest rate on your car loan, and then use that information to estimate your interest payments.

To calculate the periodic interest rate, you need to know the annual percentage rate (APR) and the number of periods in the loan. The APR is the annual rate charged for borrowing, expressed as a percentage of the principal loan amount. It includes any fees or additional costs associated with the loan.

For example, let’s say you have a $10,000 car loan with an APR of 5% and a term of 48 months. The periodic interest rate would be:

5% / 12 periods = 0.04167% or 0.004167 rounded to three decimal places

To calculate your total interest payments, you need to multiply the periodic interest rate by the total number of periods in the loan. In this example, that would be:

0.004167 x 48 periods = 2% or $200 in interest charges

Determine the number of payments

You’ll need to know the number of payments you’ll be making on your car loan in order to use the formula. The number of payments you’ll make is determined by the length of your loan. For example, if you have a four-year loan, you’ll make 48 payments (12 payments per year times 4 years). If you have a five-year loan, you’ll make 60 payments, and so on.

Multiply the loan amount by the periodic interest rate

Assuming that you’re trying to calculate the interest that will accrue on your car loan, you’ll need to follow these steps:

1. Determine the amount of your loan. This is the principal amount.

2. Determine the periodic interest rate. This is the rate that will be used for each payment period and is usually given as a decimal. For example, a 5% interest rate would be0.05.

3. Multiply the loan amount by the periodic interest rate. The result is the amount of interest that will accrue for one payment period.

4. To get the total amount of interest that will accrue on your loan, you’ll need to multiply the result from step 3 by the total number of payment periods in your loan term.

Multiply the result by the number of payments

After you’ve determined the interest rate, you’ll need to multiply it by the amount of time that you’ll be making payments on the loan. For example, if you’re taking out a five-year loan, you’ll need to multiply the interest rate by 60 (5 years x 12 months = 60 months).

Divide the result by the number of payments

After you’ve determined the interest rate and the loan amount, you can use the following formula to figure the interest payment for any car loan:

I = Prt

where I stands for interest, P stands for principal (the original loan amount), r stands for the interest rate, and t stands for the number of payments.

To use this formula, simply plug in the appropriate numbers. For example, let’s say you took out a $15,000 car loan with a 4% interest rate. You would have 60 payments of $377.42 each.

I = 15,000 x 0.04 x 60

I = 15,000 x 0.0024

I = $360

Add the result to the loan amount

To calculate the total amount you will pay on your loan, you will need to add the interest to the loan amount. The easiest way to do this is to use the formula:

Total Amount = Loan Amount + (Loan Amount * Interest Rate)

For example, if you have a $20,000 loan with an interest rate of 3%, your total amount would be $20,600 ($20,000 + $600).