How to Avoid Interest on Your Credit Card

Contents

It’s important to understand how to avoid interest on your credit card so that you can keep your finances in order. By following these simple tips, you can avoid paying interest on your credit card and keep your money where it belongs – in your pocket!

Checkout this video:

Introduction

Credit cards can be a great way to finance purchases or consolidate debt. However, if you don’t pay your balance in full each month, you will be charged interest on the outstanding balance.

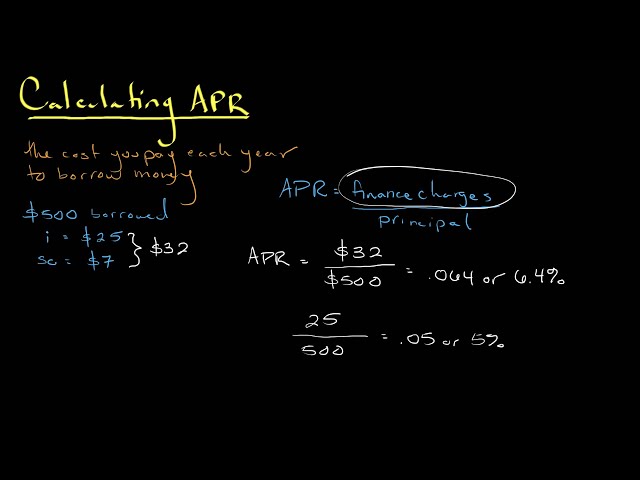

Interest is the cost of borrowing money, and is typically expressed as a percentage of the total amount borrowed. For example, if you have a credit card with an annual percentage rate (APR) of 18%, and you carry a balance of $1,000, you will be charged $180 in interest over the course of one year.

There are several ways to avoid paying interest on your credit card:

– Pay your balance in full and on time each month. This is the best way to avoid paying interest, as you will only be charged for purchases made in the previous billing cycle.

– Use a 0% APR introductory offer. Many credit cards offer 0% APR for a set period of time (usually 12-18 months), which means you will not be charged any interest on purchases made during that time frame. Be sure to pay off your balance before the intro period ends, as any remaining balance will be subject to the standard APR.

– Transfer your balance to a 0% APR credit card. If you have an existing balance on another credit card with a high APR, you can transfer that balance to a new card with a 0% intro APR offer. This can help you save on interest charges while you work to pay off your debt. Just be sure to read the terms and conditions carefully, as some offers may come with balance transfer fees.

– Take advantage of grace periods. Most credit cards offer a grace period of 21 days after the close of each billing cycle during which no interest will accrue on new purchases. If you pay yourbalance in full and on time each month, you can avoid paying interest altogether.

– Negotiate with your credit card company. If you have been a good customer and have always paid your bill on time, call your credit provider and ask for a lower APR. They may be willing to work with you to lower your rate and help keep your business.

What is Interest?

Interest is the cost of borrowing money, and it’s charged as a percentage of your outstanding balance. For example, if you have a credit card with a $1,000 balance and an annual percentage rate (APR) of 15%, you’ll owe $150 in interest at the end of the year. The higher your APR, the more interest you’ll pay.

There are two types of interest: simple and compound. Simple interest is calculated based on the principal, or the initial amount you borrowed. Compound interest is calculated based on the principal and also on the accumulated interest of previous periods.

Most credit card companies calculate interest using the average daily balance method, which means that they take the sum of your balance each day in a billing period and divide it by the number of days in that period. This produces your average daily balance, which is then used to calculate your interest charge for the next billing cycle.

How to Avoid Interest

If you are carrying a balance on your credit card, you are probably paying interest on that balance. Interest is the cost of borrowing money, and it is expressed as a percentage of the balance you owe. For example, if you have a credit card with an annual percentage rate (APR) of 18%, you will be charged 18% interest on any balance you carry from one month to the next.

Pay Your Balance in Full

The best way to avoid interest on your credit card is to pay your balance in full each month. That way, you won’t be charged any interest.

If you can’t pay your balance in full, you should try to pay as much as possible. The more you can pay, the less interest you’ll have to pay.

Some credit cards offer 0% APR for a certain period of time. This can be a good option if you know you’ll be able to pay off your balance before the 0% APR period ends. Just be sure to read the fine print so you know what the terms are.

Another option is to transfer your balance to a card with a lower APR. This can save you money on interest, but it’s important to make sure you understand the terms before you transfer your balance. Some cards have balance transfer fees, and some have introductory rates that go up after a certain period of time.

You can also try negotiating with your credit card company to get a lower APR. If you have a good payment history and your credit score is good, they may be willing to lower your APR. It never hurts to ask!

Use a 0% APR Credit Card

If you have good credit, you may be able to find a 0% APR credit card to use for your purchase. This means that you won’t have to pay any interest on your balance for a set period of time, usually between 12 and 21 months.

This can be a great way to save money on interest, but you need to be sure that you can pay off your balance before the intro period ends. If you can’t, you’ll be stuck paying interest at the regular APR, which is usually around 16%.

Use a Credit Card with a Low Interest Rate

If you’re planning to carry a balance on your credit card, it’s important to choose a card with a low interest rate. Otherwise, you’ll end up paying more in interest than you would have with a higher-rate card.

To find a low-interest credit card, compare the annual percentage rates (APRs) of several cards before you apply. You can also look for cards that offer introductory rates for balance transfers or purchases. Just be sure to read the fine print so you know how long the introductory rate will last and what the regular APR will be after that.

Once you’ve found a low-interest credit card, use it wisely by making payments on time and in full each month. This will help you avoid interest charges and keep your account in good standing.

Conclusion

Paying your credit card bill in full and on time is the best way to avoid interest charges.

If you can’t pay your balance in full, try to at least pay the minimum amount due by the due date. This will help you avoid late fees and keep your account in good standing.

If you’re struggling to make payments, contact your credit card issuer to discuss your options. They may be able to work with you to create a payment plan or lower your interest rate.