How to Use a Loan Calculator to Pay Off Your Loan Faster

Contents

A loan calculator can help you see how extra payments can help you pay off your loan faster. You can use a loan calculator to estimate your monthly payments and see how much you could save by making additional payments.

Checkout this video:

Introduction

A loan calculator can help you pay off your loan faster. By entering some basic information about your loan, such as the interest rate and the term of the loan, you can calculate how much you will need to pay each month to pay off the loan early.

There are a number of online calculators that you can use, or you can use a spreadsheet program to set up your own calculator. The important thing is to make sure that you include all of the necessary information so that you can get an accurate calculation.

Once you have calculated your monthly payment, you can start making extra payments towards your loan. By doing this, you will reduce the amount of interest that you accrue on the loan, and you will also shorten the term of the loan.

Making extra payments on your loan is one of the best ways to save money and pay off your debt sooner. If you are not sure how much extra you can afford to pay each month, start with a small amount and increase it as you are able. Making even a few extra dollars each month can make a big difference in how quickly you pay off your debt.

What is a Loan Calculator?

A loan calculator is a simple tool that will allow you to see how much money you can save by paying off your loan early. It will also help you determine the best way to pay off your loan so that you can save the most money.

To use a loan calculator, you will need to know the following information:

-The amount of money you borrowed

-The interest rate on your loan

-The term of your loan

-Your current monthly payment amount

With this information, you can plug it into the loan calculator and it will show you how much money you can save by paying off your loan early. It will also show you the best way to pay off your loan so that you can save the most money.

How to Use a Loan Calculator

A loan calculator is a great way to figure out how much you can afford to pay on your loan each month. By inputting your loan amount, interest rate, and loan term, you can calculate your monthly payment and see how much interest you will pay over the life of the loan. A loan calculator can also help you make a budget and see how much money you need to save each month to pay off your loan faster.

Estimate your monthly loan payments

A loan calculator is a simple tool that will allow you to predict how much a personal loan will cost you as you pay it back every month. You’ll just need to input a few details about the loan, and the calculator will do the rest.

To use a loan calculator, you’ll need to know four key pieces of information:

-The amount of money you need to borrow (the principal)

-The length of time you’ll need to pay back the loan (the term)

-The interest rate on the loan

-Whether the interest on the loan is fixed or variable

With this information, a loan calculator can estimate your monthly payments, as well as the total amount of interest you’ll pay over the life of the loan. Estimating your monthly payments can help you decide whether a personal loan is right for you, and if so, how much you can afford to borrow.

To find a personal loan that fits your needs, compare personal loans from multiple lenders. Once you’ve found a few personal loans with competitive interest rates and terms, use a loan calculator to estimate your monthly payments for each one.

Determine the interest you will pay over the life of the loan

In order to calculate the amount of interest you will pay over the life of your loan, you will need to know the loan’s APR. The APR (annual percentage rate) is the yearly rate of interest that is paid on a loan, and it can vary greatly from one lender to another. To calculate the amount of interest you will pay over the life of your loan, you will need to multiply the loan’s APR by the total number of years you have to pay off the loan. For example, if you have a 5-year loan with an APR of 10%, you will pay $500 in interest over the life of the loan.

Use the loan calculator to create a debt payoff plan

When you’re trying to pay off a loan, it’s important to create a debt payoff plan. A loan calculator can help you figure out how much you need to pay each month to pay off your loan by a certain date.

Here’s how to use a loan calculator to create a debt payoff plan:

1. Enter the loan amount, interest rate, and repayment term into the loan calculator.

2. The calculator will give you your monthly payment amount.

3. Make sure you can afford the monthly payment amount. If not, adjust the loan amount, interest rate, or repayment term until you find a monthly payment amount you can afford.

4. Once you find a monthly payment amount you can afford, enter that into the “Monthly Payment” field in the calculator.

5. Enter the date you want to be debt-free into the “Payoff Date” field in the calculator.

6. The calculator will show you how much money you need to save each month to reach your goal.

7. Start saving!

Conclusion

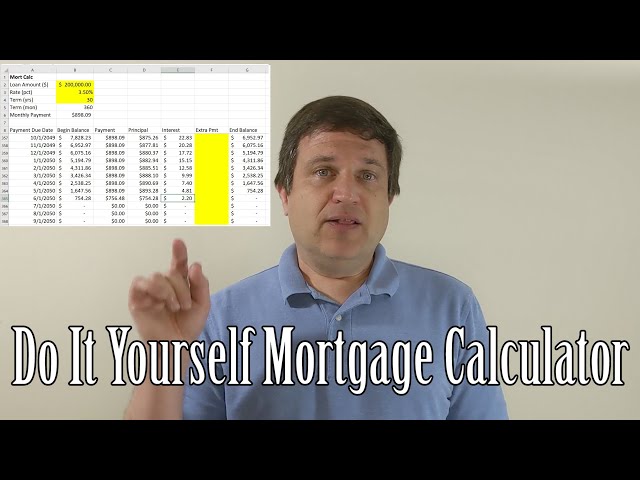

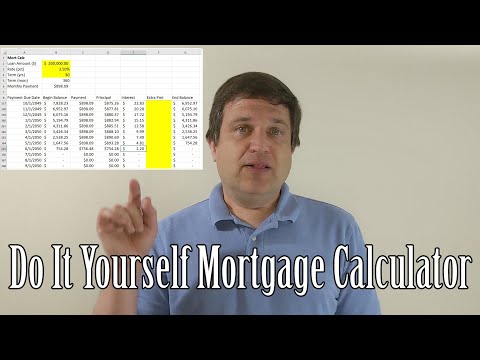

The example above shows that by making small extra payments each month, you can pay off your loan much faster than by making only the required monthly payments. In fact, you’ll save over $15,000 in interest and shave almost four years off the life of your loan.

If you have a loan with a higher interest rate, the savings will be even greater. And, if you can afford to make even larger extra payments, you’ll get out of debt even faster.

Making extra payments isn’t always easy, but it’s worth trying if you want to get out of debt as quickly as possible. And, using a loan calculator like the one above can help you see exactly how much you’ll save by making additional payments.