How Long Do I Have to Dispute a Credit Card Charge?

Contents

Wondering how long you have to dispute a credit card charge? We’ve got the answer, along with some helpful tips on what to do if you spot a fraudulent charge on your card.

Checkout this video:

The Fair Credit Billing Act

What is the Fair Credit Billing Act?

The Fair Credit Billing Act is a federal law that protects consumers from unfair credit card billing practices.

The FCBA gives consumers the right to dispute unauthorized charges or billing errors, and requires credit card companies to respond to disputes within 30 days. If the credit card company finds in favor of the consumer, the company must refund the disputed amount, plus any interest that may have accrued.

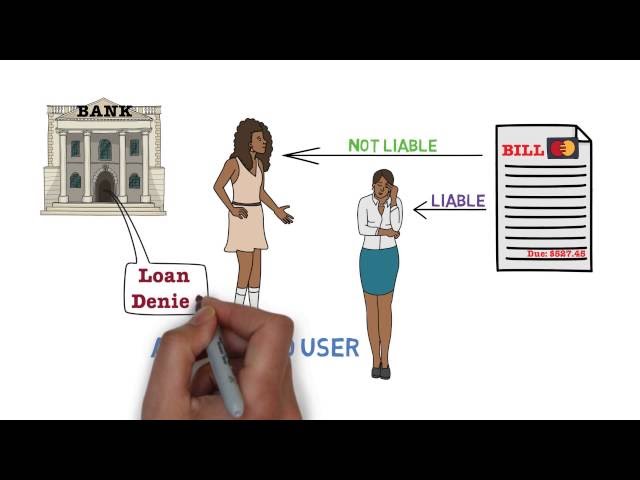

The FCBA also limits a consumer’s liability for unauthorized charges to $50.

How does the Fair Credit Billing Act protect consumers?

The Fair Credit Billing Act is a federal law that gives consumers the right to dispute unauthorized charges on their credit card bills, and requires creditors to respond to disputes within 30 days. The law also limits consumers’ liability for unauthorized use of their credit cards to $50.

In the event that you do not receive a response from your creditor within 30 days, you have the right to file a written notice with the creditor, outlining the charges that you dispute. The creditor must then investigate the disputed charges and correct any errors within two billing cycles (but no more than 90 days). If the creditor is unable to verify that the charges are accurate, they must remove them from your bill.

The Fair Credit Billing Act provides important protections for consumers, but it is important to note that it only applies to credit card purchases –– not debit card transactions or checks. Additionally, the Act does not apply to disputes over services that have been provided (such as a hotel stay or car rental), only to billing errors.

How to dispute a credit card charge

If you’ve been charged for something you didn’t purchase, you have the right to dispute the charge with your credit card issuer. You should notify your issuer as soon as possible after you see the charge on your statement. By law, they have to investigate and respond to your claim within 30 days.

How to file a dispute

If you see a charge on your credit card that you don’t recognize, or if you believe you’ve been overcharged for a purchase, you can file a dispute with your credit card issuer.

In order to file a dispute, you’ll need to contact your credit card issuer and provide them with some basic information about the charge in question. You can usually do this by phone, but some issuers also allow you to file a dispute online.

Once your credit card issuer receives your dispute, they will open an investigation and will typically contact the merchant on your behalf to try to resolve the issue. If the merchant is unable to provide evidence that the charge is legitimate, then the issuer will generally refund the amount of the disputed charge to your account.

It’s important to note that you generally have only a limited time period in which to file a dispute—typically 60 days from the date of the statement on which the disputed charge appears. So if you see a suspicious charge on your statement, don’t delay in contacting your issuer to report it.

What happens after you file a dispute?

If you dispute a credit card charge for any reason and the card issuer finds in your favor, you are not responsible for the charge. If the card issuer finds in the merchant’s favor, you may still have to pay the charge, but you may be able to get a refund if you used a debit card.

The first thing that happens when you file a dispute is that the credit card issuer investigates your claim. The issuer will contact the merchant and ask for documentation to support the charge. The merchant has 10 days to respond.

If the merchant does not respond or if the documentation is not sufficient, the issuer will likely refund your money. If, however, the documentation is sufficient or if the merchant provides enough evidence to support the charge, you may be responsible for paying it.

If you used a debit card, you may also be able to get a refund if you can show that the purchase was unauthorized or that you were charged twice for the same purchase.

How long do you have to dispute a credit card charge?

If you have a credit card and you make a purchase using that credit card, you have the right to dispute the charge if you feel like you were wrongfully charged. You can dispute the charge with your credit card company, and if they agree that you were wrongfully charged, they will refund your money. Most credit card companies have a time limit for how long you have to dispute a charge, so it is important to know how long you have.

When does the clock start ticking?

There is no universal answer to this question since credit card companies all have their own policies. However, in general, you have between 60 and 120 days from the date of the transaction to file a dispute.

If you spot a fraudulent charge on your credit card statement, the first thing you should do is contact your credit card issuer. They will usually be able to help you resolve the issue without filing a dispute. However, if you are unable to reach a resolution, you can file a dispute with your credit card company.

When filing a dispute, be sure to include any relevant documentation, such as a copy of the credit card statement showing the disputed charge. You should also include a detailed explanation of why you are disputing the charge. Once the credit card company receives your dispute, they will investigate and determine whether or not to refund the charged amount.

It is important to note that while you are disputing a charge, you are still responsible for paying the remainder of your bill. If you do not pay your bill in full, you may be subject to late fees and other penalties.

What if the dispute is not resolved in your favor?

If you do not agree with the credit card issuer’s decision, you can file a statement with your credit card company explaining why you disagree. This is called a “billing error notice.” The credit card issuer must acknowledge your billing error notice within 30 days, unless they send you a notice that they need more time to investigate. The credit card issuer must resolve the dispute within two billing cycles (but not more than 90 days) after receiving your billing error notice.

Tips for disputing a credit card charge

Keep good records

If you plan to dispute a charge, be sure to keep detailed records of your correspondence with the credit card company, as well as any supporting documentation. This could include copies of bills, receipts, or other proof that you attempted to resolve the issue with the merchant.

The credit card company may require you to submit your documentation in writing, so it’s a good idea to have everything organized and ready to go before you start the dispute process.

Be polite

When you call your credit card issuer, be calm and polite. Ranting and raving will not get you anywhere.

Credit card customer service representatives are people too, and they are more likely to help you if they like you. So be nice!

Be persistent

If you’re disputing a charge with your credit card issuer, be persistent. Call as soon as you see the charge on your statement and follow up in writing. Be sure to include your account number, the date of the purchase and a description of the problem.

If you’ve tried to resolve the issue with the merchant and it hasn’t worked, ask your credit card issuer to remove the charge. Depending on the issuer’s policies, you may have to wait until you receive your next statement before the charge is removed.

If you don’t see a credit on your next statement, call customer service and ask for a supervisor. Be prepared to provide documentation of your dispute, such as copies of correspondence with the merchant or details of any phone conversations.

It may take a few phone calls and some persistence, but disputing a credit card charge is usually worth the effort.