How High Do Credit Scores Go?

Contents

A credit score is a numerical expression based on a level analysis of a person’s credit files, to represent the creditworthiness of an individual.

Checkout this video:

Introduction

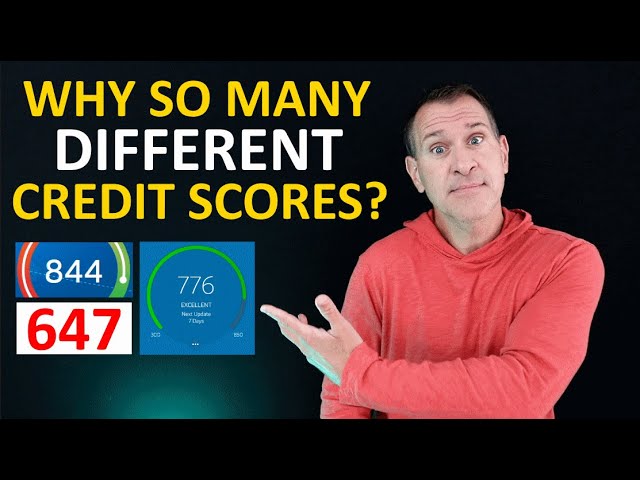

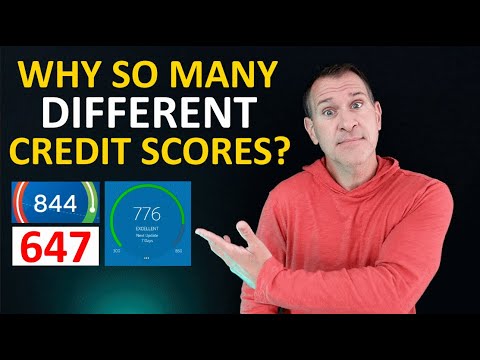

Credit scores range from 300-850. The higher the score, the better your credit is perceived to be by potential lenders. Excellent credit is typically around 800 and above. Good credit is usually in the 720-779 range. Fair credit is generally 640-699. Poor or bad credit is anything below 640. Negative marks on your credit report, such as late or missed payments, can cause your score to drop significantly.

What is a credit score?

A credit score is a number that lenders use to evaluate your creditworthiness. It’s a way for them to determine whether you’re likely to repay your debts on time. The higher your score, the better your chances of getting approved for a loan or line of credit.

scores range from 300 to 850, and the higher the score, the better. If you have a score of 760 or higher, you’re in good shape. A score between 700 and 759 is considered fair, while anything below 700 is considered poor.

There are a few things you can do to improve your credit score, such as paying your bills on time, maintaining a good credit history, and using less than 30% of your available credit.

Factors that affect credit scores

Credit scores range from 300-850. The average credit score is 687. Factors that affect your credit score include your payment history, credit utilization, credit mix, and length of credit history. Let’s take a closer look at each one.

Payment history

Most people know that paying their bills on time is important to maintaining a good credit score. Just one late payment can have a negative impact on your score, and the effects can last for years. That’s why it’s important to always pay at least the minimum amount due by the due date. If you can’t pay the full amount, call your creditor and try to work out a payment plan.

Your payment history makes up 35% of your FICO® Score—that’s almost one-third, so it’s pretty important. Payment history includes things like whether you pay your bills on time, and if you have any collection accounts or bankruptcies in your past.

If you have any delinquent accounts, it’s important to get them current as soon as possible and keep them current going forward. derogatory items, like late payments, collections and bankruptcies, can stay on your credit report for up to 10 years, but their impact on your credit score will lessen over time. So, even if you have some blemishes in your payment history, don’t despair—positives like a long history of paying on time will offset those negatives after a few years.

Credit utilization

Your credit utilization ratio is the proportion of your total credit limit that you’re using at any given time. It’s one of the most important factors in your credit score, and it’s something you can control.

A high credit utilization ratio can harm your credit score. It’s generally best to keep your ratio below 30%. If you have a high balance on one or more cards, try to pay it down as quickly as possible. You can also ask your card issuer for a higher credit limit, which will lower your credit utilization ratio.

Your credit utilization ratio is different from your total debt. Your total debt is the amount you owe on all of your accounts, while your credit utilization ratio is the proportion of your total credit limit that you’re using at any given time.

Length of credit history

One important factor that affects your credit score is your length of credit history, or how long you have been using credit. This makes up 15% of your FICO® Score.

The calculation for this factor considers the age of your oldest account, the average age of all your accounts and how recently you have used certain accounts. So, even if you have just a few accounts open, having older accounts will help increase your score in this category.

You can improve your length of credit history by keeping old accounts open and active. You could also consider opening a new account to add to the average age of all your accounts, but keep in mind that this will result in a hard inquiry on your report, which could temporarily lower your score.

Types of credit

Credit mix— including different types of credit accounts in your credit report—is one of the many factors that can influence your credit scores.

While having a variety of credit types may improve your credit mix and expand your borrowing options, you don’t need to have all types of accounts to build good credit. And, having a lot of accounts open at once could actually lower your credit scores because it might look like you’re trying to access too much credit at once.

Here are some common types of credit:

-Installment loans. An installment loan is a loan with fixed payments and a set number of payments over a set period of time. A mortgage is an example of an installment loan.

-Revolving debt. Revolving debt, such as a credit card balance, doesn’t have a set number of payments or payoff date. The monthly payment amount varies depending on the balance, interest rate and minimum payment required by the lender.

-Mortgages

-Auto loans

-Student loans

-Personal loans

-Lines of credit

How high do credit scores go?

It’s a common question: “What is the highest credit score possible?” And unfortunately, there is no one definitive answer.

Credit scores range from 300 to 850, and the higher the score, the better. However, there are a number of factors that can influence your score, including your payment history, credit utilization, and length of credit history. So while there is no single highest credit score possible, there are things you can do to improve your score and make it as high as possible.

Payment history is one of the most important factors in your credit score, so it’s important to always pay your bills on time. You should also try to keep your credit utilization low; experts recommend using no more than 30% of your available credit. Finally, a longer credit history will also help boost your score. So if you have a good payment history and low credit utilization, you’re on the right track to getting a high credit score.

Conclusion

Based on the information we’ve gathered, it seems that credit scores can go as high as 850. However, it’s important to remember that credit scores are constantly changing, so this number is subject to change. In addition, there are many different types of credit scores out there, so not all 850s will be created equal.