How Does a Loan Work?

Contents

If you’re considering taking out a loan , you’re probably wondering how they work. In this blog post, we’ll explain how loans work, what you need to qualify, and some of the pros and cons to help you make a decision.

Loan Work?’ style=”display:none”>Checkout this video:

Introduction

A loan is a type of borrowing in which you agree to borrow a certain amount of money, over a set period of time, and with certain conditions attached. You then repay the borrowed amount, plus interest, over the life of the loan.

Loans can be used for a variety of purposes, including buying a car or home, paying for education or medical expenses, or starting a business.

There are two main types of loans: secured and unsecured. With a secured loan, you put up collateral — such as your home or car — as insurance against defaulting on the loan. Unsecured loans don’t require collateral, but they may have higher interest rates and penalties if you don’t make your payments on time.

Before you take out a loan, it’s important to understand how they work and what the terms and conditions are. This will help you make the best decision for your needs and avoid any unwanted surprises down the road.

How Does a Loan Work?

A loan is a sum of money that is given to an individual or a business by a financial institution. The recipient of the loan is then obligated to repay the loan , plus interest , over a set period of time. There are many different types of loans, such as mortgages, auto loans, and personal loans.

The Basics of a Loan

In order to understand how a loan works, it is important to first understand the different types of loans available. The two most common types of loans are secured and unsecured loans.

A secured loan is a loan in which the borrower pledges an asset (such as a car or property) as collateral for the loan. This means that if the borrower defaults on the loan, the lender can seize the collateral to recoup their losses. Secured loans tend to have lower interest rates than unsecured loans because they are less risky for lenders.

An unsecured loan is a loan that is not backed by collateral. This means that if the borrower defaults on the loan, the lender cannot seize any assets. Unsecured loans tend to have higher interest rates than secured loans because they are more risky for lenders.

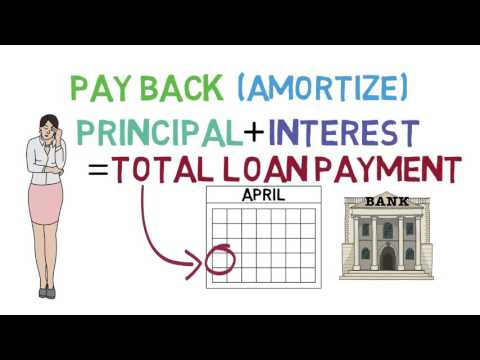

The term of a loan is the amount of time that a borrower has to repay the loan. The most common Loan terms are 5 years, 10 years, and 20 years. The interest rate is the amount of interest that will be charged on the outstanding balance of the loan. Interest rates can be fixed or variable. A fixed interest rate means that the interest rate will not change during the term of the loan. A variable interest rate means that the interest rate will change during the term of the loan based on changes in an underlying index, such as the prime rate.

The monthly payment on a loan is determined by four factors:

-the amount borrowed (the principal);

-the term of the loan;

-the interest rate; and

-whether payments are made monthly, quarterly, or annually.

For example, let’s say you borrow $1,000 at an annual percentage rate (APR) of 5% for two years with monthly payments. Your monthly payment would be $43.21 ($1,000 x 0.05 / 12 months). At the end of two years, you would have paid $1,038 in interest ($43.21 x 24 payments).

The Application Process

The first step in the loan application process is to fill out a loan application form. This form will ask for information about your employment, income, debts, and other financial information. Once you have completed the form, a lender will review your information and make a decision about whether or not to approve your loan.

If you are approved for a loan, the next step is to sign a loan contract. This contract will outline the terms of your loan, including the interest rate, repayment schedule, and other important details. Once you have signed the contract, you will then need to make a down payment on the loan. After you have made your down payment, the lender will disperse the funds to you.

The Types of Loans

Most people think of loans as a way to get cash for a big purchase, like a car or a house. But there are other types of loans, like student loans and business loans. Each type of loan has its own terms and conditions.

Most loans are made by banks and credit unions, but there are other ways to get a loan, too. Here are some common types of loans:

Auto Loans

Auto loans are used to finance the purchase of a new or used vehicle. The loan is secured by the vehicle, which means that if you can’t make your payments, the lender can repossess the car. Auto loans typically have terms of 36 to 60 months (3 to 5 years).

Home Loans

Home loans are used to finance the purchase or construction of a home. The loan is secured by the home, which means that if you can’t make your payments, the lender can foreclose on your home. Home loans typically have terms of 15 to 30 years.

Student Loans

Student loans are used to finance the cost of higher education. The loan is usually repaid after you graduate from college, although some student loans have terms of 10 to 20 years. Student loans typically have lower interest rates than other types of loans because they’re considered “good debt.”

Business Loans

Business loans are used to finance the start-up or expansion of a business. The loan is usually secured by collateral, such as equipment or inventory. Business loans typically have terms of 5 to 10 years.

Conclusion

In conclusion, loans can be a great way to finance a large purchase or cover unexpected expenses. But it’s important to understand how they work before you apply for one. Be sure to shop around and compare offers from multiple lenders to get the best deal. And remember, always read the fine print carefully before you sign any loan agreement.