How Does Your Credit Score Work?

Contents

Want to know how your credit score works and what you can do to improve it? Check out this blog post for everything you need to know!

Credit Score Work?’ style=”display:none”>Checkout this video:

What is a credit score?

A credit score is a number that lenders use to decide whether or not to lend you money. It is based on your credit history, which is a record of how you have handled borrowing and repaying in the past. The higher your score, the more likely you are to be approved for a loan or credit card and to get a lower interest rate.

Credit scores are used by lenders as one way to determine whether or not you are a good candidate for a loan. However, there are other factors that lenders will consider, such as your employment history and income.

There are many different types of credit scores, but the most common one is called the FICO score. This score ranges from 300 to 850, and the higher your score, the better. Scores below 650 are considered poor, and scores above 700 are considered excellent.

If you’re not sure what your credit score is, you can check it for free on several websites, including CreditKarma.com and CreditSesame.com.

How is your credit score calculated?

Your credit score is calculated using information from your credit report . This information is used to determine your creditworthiness. Factors that are considered include your payment history, outstanding debt, credit utilization, credit mix, and length of credit history.

Payment history

One of the biggest factors in your credit score is whether you pay your bills on time. Specifically, it’s the record of whether you’ve made payments within the last two years.

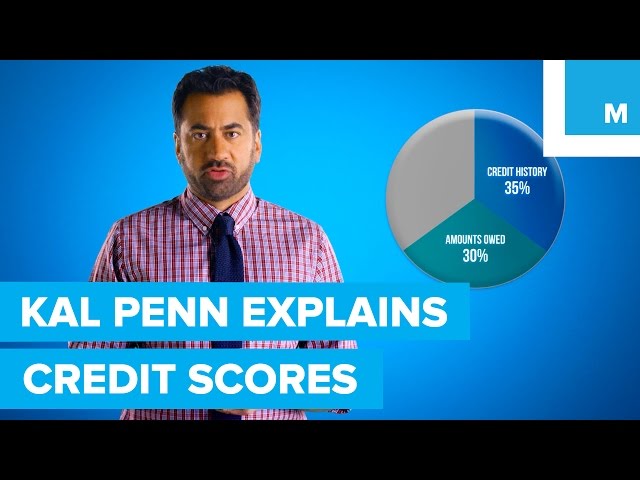

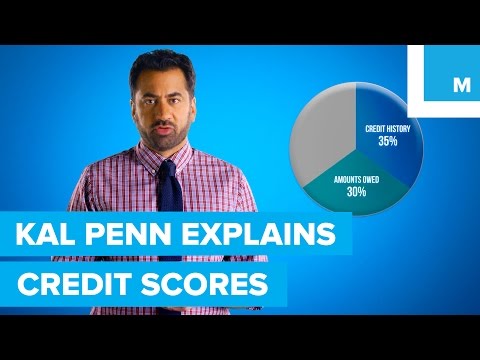

Your payment history makes up 35% of your FICO credit score, so it’s clearly important. The weight given to late payments diminishes with time, so even if you have a history of late payments, as long as you’ve been paying on time for a while, your credit score will gradually improve.

However, if you have a recent late payment, that can have a significant negative effect on your score. So if you’re trying to improve your credit score, one of the best things you can do is make sure you always pay your bills on time.

Credit utilization

Credit utilization is one of the biggest factors in your credit score—accounting for about 30% of your FICO® credit score.1 That’s because it provides creditors with an indication of how much of your available credit you are using. Creditors like to see that you’re not maxing out your credit cards, because that could indicate financial stress.

Generally speaking, using less than 30% of your available credit should help your credit utilization rate, and therefore, your credit score. If you have a $1,000 credit limit and carry a balance of $300, for example, your credit utilization rate would be 30%. The lower your rate is, the better it will be for your score.

Length of credit history

One of the biggest factors in your credit score is the length of your credit history. As a general rule, the longer you’ve been borrowing money and paying it back on time, the better. This is why it’s important to start building credit as early as possible.

That said, there are a few things that can shorten your credit history, including closing old accounts or opening new ones too often. So even if you have a long history of using credit responsibly, making some changes to your credit habits can still negatively impact your score.

Other factors that affect your credit score include:

-Payment history: This is a record of whether you’ve made your payments on time. Late or missed payments will hurt your score.

-Credit utilization: This is the amount of debt you have compared to the amount of credit available to you. It’s important to keep this number low — ideally below 30% — because lenders will see you as a higher risk if you’re using a lot of your available credit.

-Credit mix: Having a mix of different types of credit (such as revolving debt like credit cards and installment debt like personal loans) can improve your score because it shows lenders that you can handle different types of borrowing.

-New credit: Opening several new accounts in a short period of time can be seen as a red flag by lenders, so try to limit the number of new accounts you open.

Types of credit

There are five types of information factoring into your credit score calculation:

-Payment history (35 percent)

-Credit utilization (30 percent)

-Length of credit history (15 percent)

-Credit mix (10 percent)

-New credit accounts (10 percent)

Your payment history is the record you’ve established by making on-time payments – or missing them. This single factor has the greatest impact on your score, so it’s important to pay all your bills on time, every time.

Credit utilization is how much debt you have compared to your credit limits. It’s calculated by adding up all your revolving debt (such as credit cards) and dividing that number by the total credit available to you. For example, if you have two credit cards – one with a $5,000 limit and another with a $10,000 limit – and you have a combined balance of $2,500, then your credit utilization ratio is 25 percent. The lower your ratio, the better for your score; most lenders like to see ratios below 30 percent.

Your length of credit history makes up 15 percent of your score. A longer history signals to lenders that you’re an experienced borrower who has managed different types of debts responsibly over time. The mix of different types of debt in your credit portfolio is worth 10 percent of your total score. That’s because having a mix demonstrates that you can handle various types of borrowing responsibly – everything from revolving debt to installment loans.

New credit accounts make up 10 percent of your total score calculation. Whenever you open a new account, it can positively or negatively affect your score depending on how it changes the rest of the factors in this equation.

How can you improve your credit score?

Your credit score is a number between 300 and 850 that lenders use to decide how likely you are to repay a loan. The higher your credit score, the more likely you are to get a loan with a lower interest rate.

Make all your payments on time

One of the most important things you can do to improve your credit score is to make all your payments on time. Payment history is the biggest factor in your credit score, accounting for 35% of your FICO® Score☉ .

If you have any late payments, get current and stay current. Once you are back on track, you may see your credit score improve. You can also get help from a credit counseling or debt management agency.

Keep your credit utilization low

Credit utilization is one of the biggest factors in credit scores, and it’s also one of the areas that consumers can easily improve.

credit utilization is the amount of revolving credit you are using divided by the total amount of revolving credit you have available. For example, if you have a $1,000 credit limit on a credit card and you owe $500, your credit utilization is 50%.

The lower your utilization ratio, the better it is for your score. In fact, certain scoring models will give you extra points for having a low credit utilization ratio. You should aim for a utilization ratio of 30% or less.

Use a mix of different types of credit

Your credit score is based on the information in your credit report. The most important factor in your credit score is your payment history—whether you pay your bills on time. The second most important factor is the amount of debt you have relative to the amount of credit you have available to you, which is called your “credit utilization ratio.”

You can improve your credit utilization ratio by using a mix of different types of credit, such as revolving credit (like a credit card) and installment loans (like a car loan). You can also improve your credit utilization ratio by paying down your debt so that you have more available credit.

Another factor that affects your credit score is the length of your credit history. So, if you have a long history of on-time payments, that will help improve your score. You can also improve your score by maintaining a good mix of different types of accounts, such as revolving and installment loans.

The final factor in your credit score is the number of recent inquiries into your report. So, if you have multiple inquiries in a short period of time, that could hurt your score. But if you have just a few inquiries over a long period of time, that will not have as much of an impact.

What are the consequences of having a low credit score?

A credit score is a number that represents the risk a lender takes when lending you money. The higher your score, the lower the risk to the lender. A low credit score can make it difficult to get approved for a loan, credit card, or mortgage. You may also be charged a higher interest rate if you are approved. A low credit score can also affect your ability to get a job or rent an apartment.

You may have difficulty getting approved for loans

If you have a low credit score, you may have difficulty getting approved for loans or credit cards. You may also be denied for certain apartments or jobs. In some cases, you may be able to get approved for a loan or credit card with a higher interest rate.

You may have to pay higher interest rates

If you have a low credit score, you may have to pay higher interest rates on loans and credit cards. This is because lenders see you as a higher risk borrower, and they want to offset that risk by charging you a higher interest rate. Higher interest rates mean that you will end up paying more money in interest over the life of the loan or credit card balance.

Another consequence of having a low credit score is that you may be turned down for loans or credit cards altogether. Lenders may not be willing to take a chance on you if your credit score is low, which can limit your access to financial products and services.

Lastly, a low credit score can make it harder to rent an apartment or get utilities turned on in your name. This is because landlords and utility companies often use credit scores as part of their decision-making process when it comes to approving applications. If your score is low, they may view you as a higher risk customer and either deny your application or charge you a higher deposit.

How can you check your credit score?

You can check your credit score by looking at your credit report.Your credit score is a number that represents your creditworthiness.It is based on your credit history, which is a record of your borrowing and repayment activities.

Check your credit report

You can check your credit report for free once a year from each of the major credit reporting agencies — Equifax®, Experian®, and TransUnion®. You can request your report online, by phone, or through the mail.

If you see any errors on your credit report, you should contact the credit bureau directly to correct them. You can also file a dispute with the credit bureau if you believe there is incorrect information on your report that you cannot resolve with the company directly.

In addition to checking your credit report, you can also track your credit score over time by signing up for a free credit monitoring service. This will give you an idea of how your score is trending and whether or not there are any red flags that you need to be aware of.

Check your credit score

Your credit score is a number that reflects the information on your credit report. Lenders use your credit score to help them decide whether to give you a loan and how much interest to charge you. You can check your credit score for free through various online services.

There are three main types of credit scoring models: FICO, VantageScore, and Experian Boost. FICO is the most common type of credit score and is used by 90% of lenders. VantageScore is the second most common type of credit score and is used by 14% of lenders. Experian Boost is the third most common type of credit score and is used by 1% of lenders.

When you check your credit score, you will likely see all three scores, as well as your average or “transunion” score, which is a combination of the three scores. It’s important to remember that each lender uses a different scoring model and weighting system, so your scores may vary depending on which lender you’re talking to.

If you’re trying to improve your credit score, there are a few things you can do: make sure your payments are on time, keep your balances low, avoid opening new lines of credit, and dispute any errors on your credit report.