How Do You Calculate a Home Equity Loan?

Contents

If you’re thinking about taking out a home equity loan, you probably want to know how much you can borrow. Here’s a quick and easy guide to help you calculate a home equity loan.

Checkout this video:

Introduction

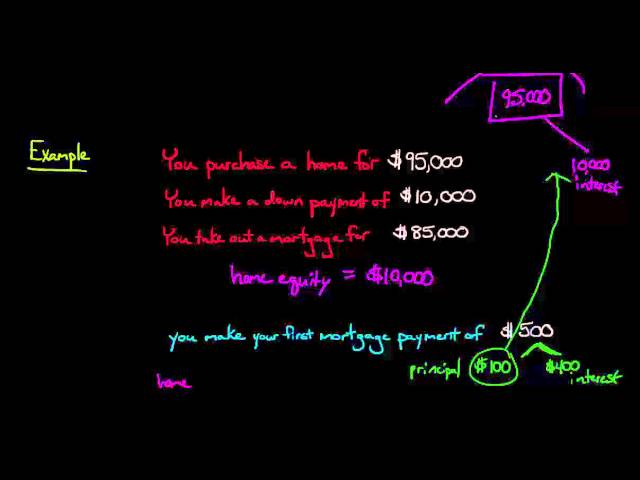

There are several ways to calculate a home equity loan, but the most common method is to take the value of your home and subtract any outstanding mortgage debts. The remaining amount is the equity that you have in your home. You can use this equity to secure a loan, which can be used for any purpose.

To calculate your equity, you will need to know the value of your home and the amount of any outstanding mortgage debts. You can find this information on your home’s deed or in your mortgage agreement. Once you have this information, you can subtract the outstanding mortgage debt from the value of your home to calculate your equity.

For example, if your home is valued at $200,000 and you have an outstanding mortgage debt of $100,000, your equity would be $100,000. You could use this equity to secure a loan for any purpose, such as making home improvements or Consolidating debt.

What is a home equity loan?

A home equity loan is a debt secured by your home that you can use for a variety of purposes, from making home improvements to consolidating other debts. The interest you pay on a home equity loan is usually tax deductible, which makes this type of loan an attractive option for many homeowners.

To calculate a home equity loan, you first need to determine the value of your home minus any outstanding mortgage debt. This will give you your equity. From there, most lenders will allow you to borrow up to 80% of your equity in the form of a loan.

For example, let’s say your home is worth $200,000 and you have a mortgage balance of $100,000. This gives you $100,000 in equity. Most lenders would then allow you to borrow up to $80,000 through a home equity loan.

The interest rate on a home equity loan is usually lower than the interest rate on a credit card or personal loan because the lender views the loan as less risky since it is secured by your house.

Home equity loans are also known as second mortgages since they are typically taken out after a first mortgage has been put in place.

How do you calculate a home equity loan?

Home equity loans are a type of loan in which the borrower uses the value of their home as collateral. The loan amount is typically based on the equity in the home, which is the difference between the appraised value of the home and the balance of the mortgage. Home equity loans can be used for a variety of purposes, including home improvements, medical bills, college tuition, or consolidating other debts.

Determine the value of your home

Before you can calculate your home equity loan, you need to know the market value of your home. This can be tricky, because sometimes your home is worth more to you than it is to someone else.

A good rule of thumb is to look at comparable homes in your neighbourhood that have recently sold, and use that as a starting point. You can also get an official evaluation from a professional appraiser. If you have a lot of unique features in your home, or if the housing market in your area has been particularly volatile, these methods may not give you an accurate number. In that case, you may want to get a comparative market analysis (CMA) from a real estate agent.

Determine the amount of equity you have in your home

To calculate a home equity loan, you will need to know the market value of your home and your outstanding mortgage balance. You can then subtract the outstanding mortgage balance from the value of your home to determine how much equity you have.

Calculate the loan amount

To calculate the loan amount, subtract the amount of equity you have from the maximum loan amount. The maximum loan amount is 90% of the appraised value of your home, minus any outstanding debt. For example, let’s say your home is worth $250,000 and you currently owe $100,000 on a first mortgage. This means you have $150,000 in equity available to use. The maximum loan amount would be 90% of $250,000, or $225,000. Subtracting the outstanding debt of $100,000 leaves a loan amount of $125,000.

Conclusion

Assuming you have a good amount of equity in your home, a home equity loan can be a great way to get a lump sum of cash for whatever purpose you need it – from debt consolidation to home improvement. As with any loan, however, it’s important to be aware of the interest rate you’ll be paying and factor that into your decision. Use our home equity loan calculator to determine how much you could borrow and what your monthly payments might be.